Ebru Boysan

Bloomberg Market Specialist

THE 50 percent dip in the price of oil during 2014-15 sent GCC countries with even the lowest break-even oil-price levels to sharp deficits after a long period of surpluses. In this article, we examine how the region is stabilizing from the shock, diversifying beyond oil and introducing the rest of its buffer zones to achieve sustainable, non-oil-driven economic growth and revenue.

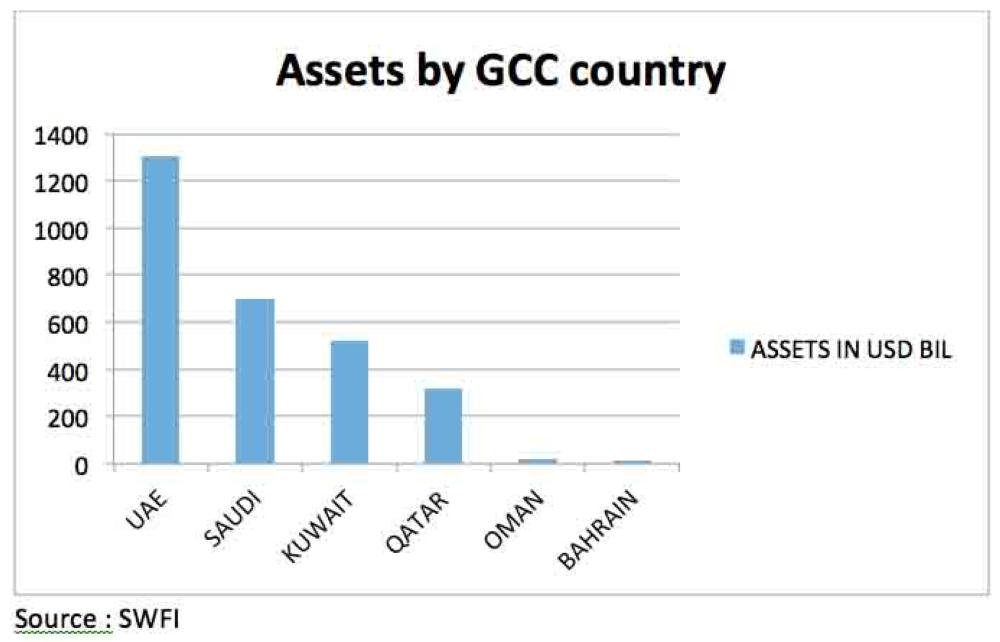

According to the Sovereign Wealth Fund Institute, GCC countries hold 40 percent of the world’s sovereign wealth fund (SWF) assets: $2.8 trillion of a $7.3 trillion worldwide total. Emirati SWFs are perfect examples of how mandates for funds can differ. The Investment Corporation of Dubai (ICD) solely focuses on the diversification of the Emirate of Dubai, which arguably leads the GCC in economic diversification. Unknown to most, other funds in the region invest directly in domestic industries to support economic diversification. A envisioned, Saudi Arabia has established the privatization of Aramco as one of its main goals, where proceeds will top up the assets of its Public Investment Fund, which could make it the biggest sovereign wealth fund in the world. This is in contrast to its previous areas of focus, predominantly private equity and domestic investments. It should be noted that SWF mandates are not to be mistaken with foreign-currency reserve management, which is held by monetary authorities with preferences towards asset allocations based on liquidity vs returns.

SWFs have historically provided liquidity to financial systems in the GCC during times of crisis. Now, SWFs in the region are undergoing structural reform, with countries such as the UAE and Qatar internally merging their respective SWFs. Moreover, central banks are playing an increasingly active role in providing liquidity for financial-system contingencies (instead of sourcing directly from SWFs in the region), which offers an additional sign of improved economic efficiency.

Population size and youth are the key ingredients of healthy domestic consumption, which in turn can play a prominent role in bolstering GCC economies. Most countries in the region, with exception of Saudi Arabia and Oman, have a relatively small native population relative to their economic ambitions. They instead rely on their expat population, with most of it holding an unclear residency status. Vulnerability lies in expat residents leaving the country, creating exposure to population shocks. Dubai in particular has seen significant exodus after the economic crisis of 2008, when working expats faced widespread redundancies.

GCC countries are now working on more long-term residency schemes to reduce volatilities of this nature. Qatar, for example, is the latest country to introduce permanent residency schemes for its expat population, while the UAE also is working on new visa schemes to attract top talent in targeted industries.

Overall, increasing economic activity, while maintaining stability, and swelling non-national population sizes will be the primary methods for the GCC to deepen local population consumption.

While tax is a major source of revenue for governments across the globe, this is not the case for the GCC. Without VAT, tracking economic activity and consumption has been challenging for economies in the region. In the absence of such data, non-standard data such as car sales, expat visas and traffic indices is analyzed instead. Six GCC countries are planning to simultaneously adopt the VAT tax in January 2018, with the rate expected to be 5 percent. Notably, the UAE is also set to implement a law that will tax tobacco products as well as energy and soft drinks in the fourth quarter of 2017.

Revenue stemming from the adoption of VAT across the region will provide a small but noteworthy contribution to GDP. Below illustrates similar VAT rates from selected peers:

Although VAT contribution may not be enormous by some standards, it will contribute to the tracking of consumption while serving as an introduction of tax in a historically tax-free region.

The GCC has historically benefitted from a large pool of capital. In recent years, mostly due to the relative size of domestic capital markets, a lot of this capital has been routed to international assets, private equity and real estate. A deeper regulatory framework is required to secure sizable asset allocation to domestic assets, provided that liquidity conditions of the assets in question are satisfactory. Implementing a stronger legal structure to minimize risk and balance long- and short-term investment goals, topped up by strong oversight to secure correct valuations, will sustain a healthy capital base that can be used to support growing domestic capital markets and assets in general.

As the GCC continues to stabilize after the oil-price drop, the world’s attention rests on the region’s ongoing structural diversification and advancement towards a sustainable future in a post-oil era.