JEDDAH — Several economies in the Middle East are set for transition in 2018, implementing new policies to tackle economic and financial vulnerabilities, and lay the ground for more diversified growth. “We expect a pickup in economic growth in the coming couple of years, but business should remain aware of risks to recovery,” the latest ICAEW Economic Insight report revealed.

In Saudi Arabia, a gradual easing in social restrictions should remove constraints to growth.

Lebanon’s economy has suffered from a combination of political upheaval and the cost of hosting 1.5 million refugees over recent years. But progress has been made on a number of fronts through 2017, and though challenges remain substantial we do expect a recovery in confidence and activity in the years ahead.

Several economies in the Middle East, particularly those in the GCC, are transitioning towards a “new normal”, and 2018 will mark some interesting milestones. Households and firms will need to adapt to the implementation of Value Added Tax, as part of a more widespread trend towards increasing government revenues from sources other than fuels. Important social change will take place in Saudi Arabia to ease barriers to economic growth and open up to the world. After a period of emergency austerity (which saw public spending cut by almost 20% from 2015-2017 at the GCC level), public finances now look to be on a more sustainable path in most economies, allowing spending to start gradually recovering, the report said.

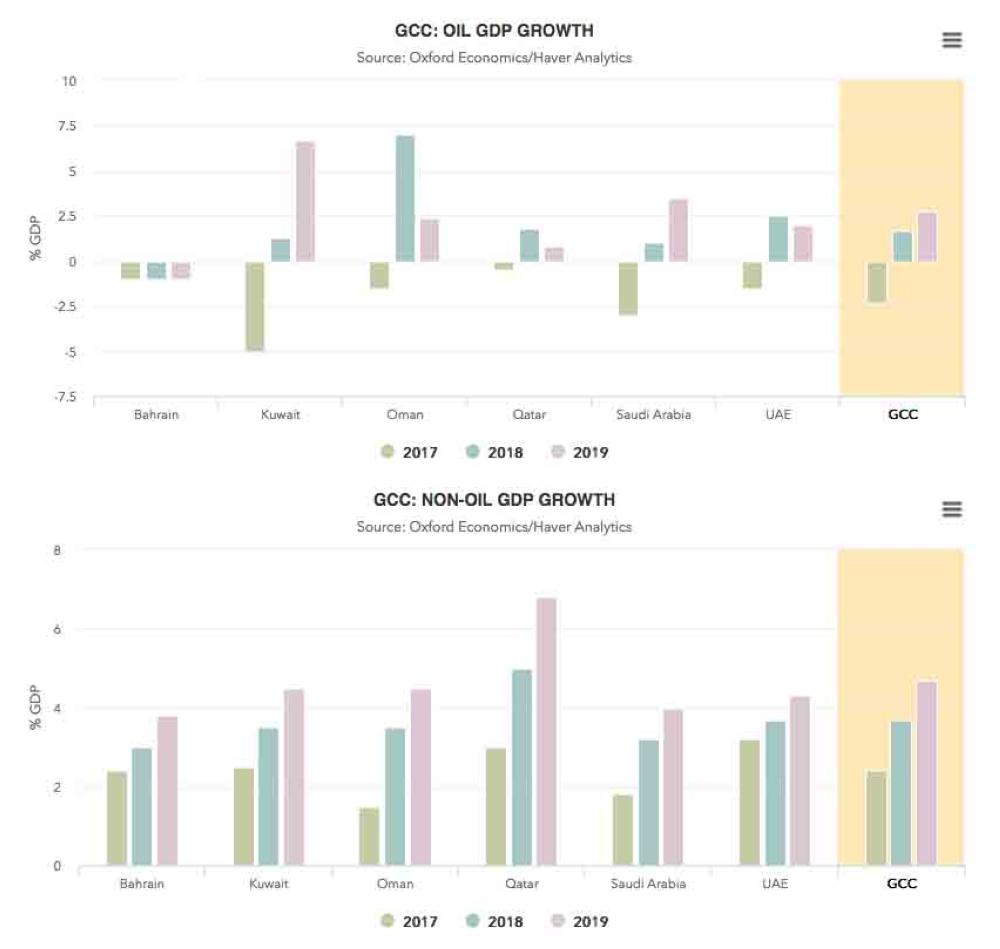

Against this backdrop, our forecast is for GDP growth in the region to recover momentum in the years ahead. “We forecast GDP growth of 2.8% in the GCC in 2018 (after growth of just 0.3% in 2017), and an acceleration from 1.4% to 3.2% in the wider Middle East.” There will remain a broad spread of growth performance though, with GCC economies bound by the OPEC agreement to keep oil output low, growing slower than other economies (although non-oil sectors are forecast to pick up).

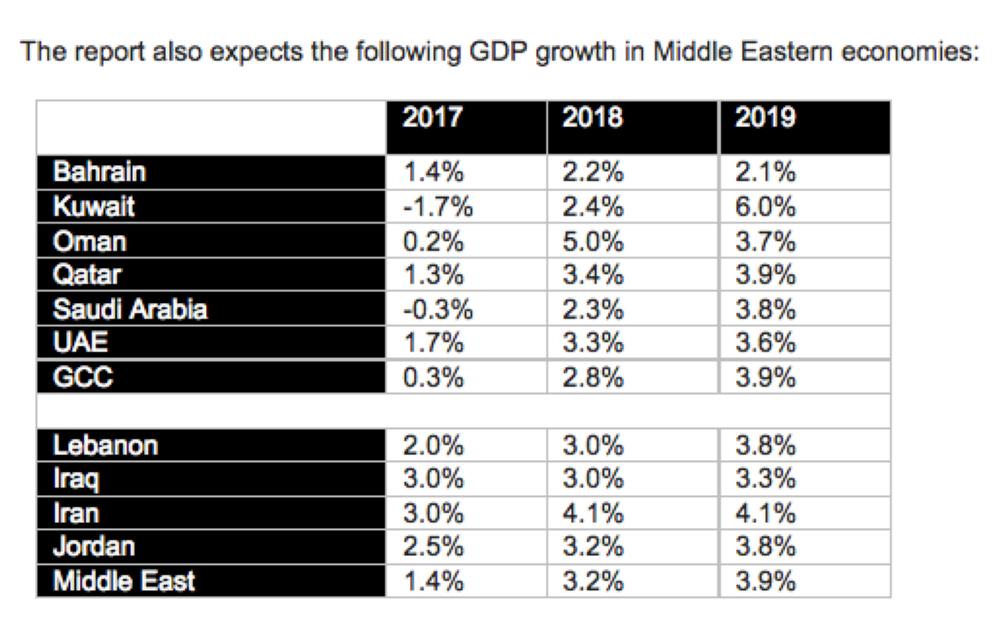

With oil production cuts likely to be maintained through 2018, and reversed in 2019, “we expect GDP growth to pick up to around 4% in both the GCC and wider Middle East. Within this, we forecast oil GDP to rebound from a 2.3% contraction in 2017 to growth of 1.7% in 2018 and around 1 percentage point stronger in 2019. Growth in the non-oil sector is forecast to pick up from 2.4% in 2017 to 3.7% in 2018 and 4.7% the year after,” the report said.

2018 will be a key year of transition for Saudi Arabia in several contexts. For the first time, Saudi citizens will pay VAT on the goods and services they buy, Saudi women will be permitted to drive, and private (and foreign) investors may be able to take a stake in Saudi Aramco. Saudi Arabia is at the start of a potentially decades-long process of economic diversification and social change.

Nevertheless, in the near-term, familiar growth drivers remain crucially important. Most obvious is Saudi Arabia’s role in rebalancing supply and demand in the world oil market. As a key player in the “OPEC-plus” coalition, Saudi Arabia has cut production by around 650,000 barrels per day (around 6%) compared to a year ago. Partly in response to the lower quotas, prices have moved higher in recent months – topping $60 per barrel for Brent crude in late October. However, demand is slowing in key markets, particularly China where the International Energy Agency expects demand growth to slow to 2.6% in 2018 (2pp slower than this year). “As such, we expect Saudi (Arabia) to play a key role in securing an extension of the lower quotas at the Nov. 30 meeting. We forecast Brent crude to average $55 in 2018 and a dollar or two higher the following year - around $5 higher than during our last forecast. This will offer some support to public spending and growth, but by no means fundamentally change the broader picture in the oil market or in Saudi Arabia specifically,” the report noted.

Away from the oil sector underlying business conditions remain relatively positive. The Emirates NBD Purchasing Managers’ Index for Saudi Arabia (a gauge of activity in the non-oil private sector) has averaged a reading of 56 for 2017 so far, compared to the “no-change” reading of 50, and an average of below 55 for 2016 overall. Private (i.e. business and households) bank deposits have also started to recover through the summer months, providing some support for spending power into 2018.

This cushion could be important, as households face a combination of additional drags on their income in 2018. Households are already dealing with the impact of cigarette and soft drink duties imposed in the summer, and these will be augmented in 2018 by the introduction of Value Added Tax, and possibly 80% hikes in motor fuels prices. More positively, plans to permit women to drive could save some households as much as $1,000 per month – particularly where women use a driver or taxis to get to their workplaces. The relaxation on women driving seems unlikely to have an immediate impact on female employment though. At 20%, female labor force participation is low even by regional standards (UAE leads the way at 42%, compared to 50-60% in western economies), and the government aims to raise this to 30% by 2030.

There is clearly increasing momentum behind the shift toward a more market-driven economy. This shift will take some time though, and for the coming years the economy will remain heavily influenced by traditional growth drivers – the oil sector, and the importance of government spending. “We forecast the economy to pick up from a 0.3% contraction in 2017 (largely a result of lower oil output) to growth of 2.3% in 2018. As oil output is restored to pre-cut levels in 2019, we expect GDP growth of 3.8%. But in the absence of more ambitious reform efforts in the coming couple of years, this is likely to be the speed limit for growth.”

Lebanon’s economy has suffered from a protracted period of below-potential growth, due to a combination of domestic political paralysis and the impact of regional conflicts, particularly in Syria. Recent political developments had yielded important improvements to policy-making. The cost of hosting 1.5 million refugees places a heavy burden on the economy, but this is likely to be offset by a rebound in key sectors as economic activity starts to pick up. “We are optimistic of a solid pickup in economic growth, from an average of just 1.7% per year from 2011-2017 to 3% in 2018, and on to 4% by 2020.”

Along with Jordan, Lebanon has been one of the most heavily-impacted countries from the crises in Syria and Iraq. Lebanon currently hosts around 1.5 million Syrian refugees (equal to around 30% of the domestic population), who have been arriving since the conflict broke out in 2011. This has put an immense strain on public finances, as the government struggles to accommodate and feed the new arrivals. Goods exports fell by 30% from 2012-2016 due to the disruption in trade, which relies predominantly on overland routes, with Lebanon’s key trade partners in the region, while tourism arrivals fell 40% between 2010-2013 (although have rebound around half-way since). Additionally, austerity measures have hit the spending power of traditionally high-spending visitors from GCC economies. The increase in public spending and contraction in revenues has driven the government budget into a deficit consistently around 10% of GDP in recent years. And while Lebanon has avoided being directly involved in the conflict, this has come at the cost of policy paralysis, with divergent views on how to deal with the crisis and Lebanon’s approach to Syria leading to the collapse of the government in 2013, further dampening business and household confidence.

Some of these pressures are starting to ease though. After more than two years without a formal head of state, Lebanon finally elected a president in October 2016, which has brought some momentum back into policy circles. Most positively perhaps parliament ratified a new electoral law in June, paving the way for elections scheduled for May 2018. Parliament also ratified the government’s budget (the first since 2005), and implemented substantial increases in public sector pay (which should help stimulate demand), paid for by increases in VAT, corporation tax and taxes on the banking sector. The resignation of the Prime Minister in early November raises the risk of a period of policy paralysis between now and the elections though. But based on the assumption the elections yield a durable government with a mandate to govern, we forecast the budget deficit to start to come down, albeit only very gradually, especially as pre-election spending may offset improvements in revenue-generation.

There are also signs of economic recovery. Tourist arrivals grew by 11% in 2016, and a further 4.6% in the first half of 2017. This is boosting activity in the sector, as well as confidence among firms more broadly. Lower oil prices are also helping, given Lebanon’s reliance on imported oil – although recent discoveries of oil and gas fields off Lebanon’s coastline will change this. Parliament recently approved a petroleum tax law, and it is hoped that production can start in 2018. Overall, assuming the election of a government with a solid mandate and that the country continues to be relatively shielded from neighboring conflicts, we feel this range of positive trends, can help push GDP growth towards 4% by 2020.

However, the new government will face several challenges in returning Lebanon to stability and prosperity. Public debt has risen to 156% of GDP, among the highest in the world, and leading ratings agencies to downgrade Lebanon to single B. Lebanon remains one of the most externally imbalanced countries in the world, with an especially severe reliance on remittances from Lebanese diaspora. This leaves the economy exposed to foreign exchange and refinancing risks. More generally, substantial economic reform is required to improve the underlying business environment – at 126 in the World Bank’s latest Doing Business ranking, Lebanon compares far from favorably with other economies in the region such as Morocco (68) and Tunisia (77). — SG