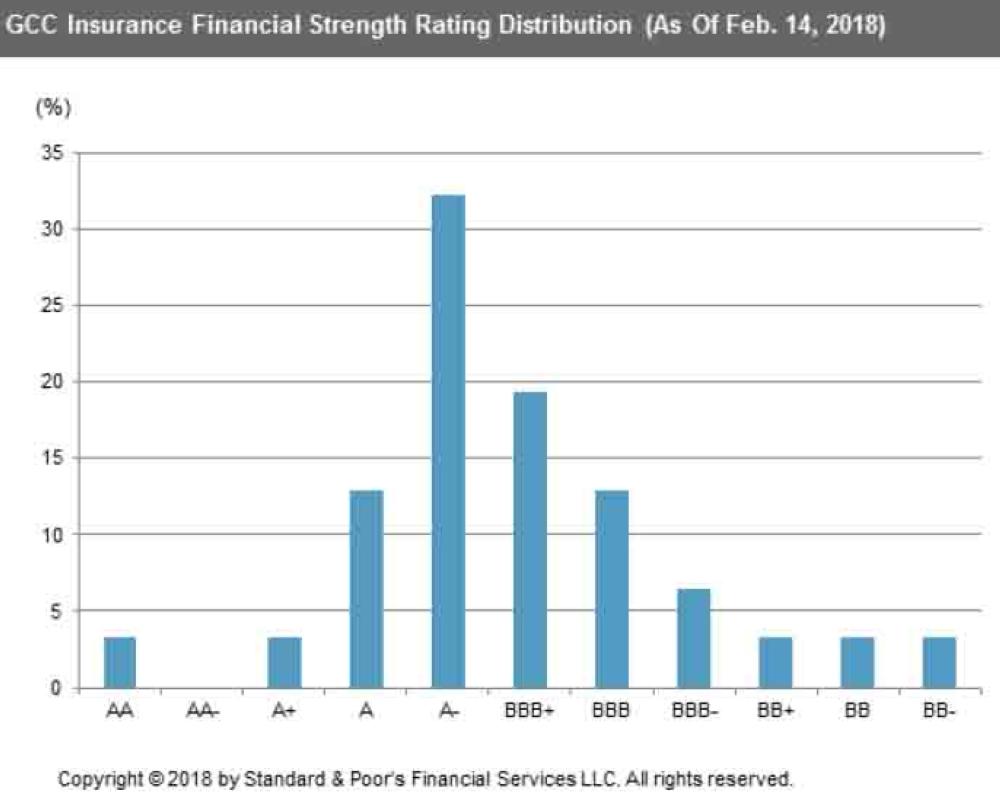

DUBAI — Despite ongoing regulatory and competitive challenges in the insurance sector in the Gulf Cooperation Council (GCC) countries, credit conditions for rated insurers will remain strong and broadly stable in 2018, according to a report published recently by S&P Global Ratings titled "Gulf Insurers: The Gap Between Big And Small Insurers Could Widen In 2018."

"New regulations with higher capital requirements and other demands will add to costs and increase pressure on profitability for some insurers, in our view," said S&P Global Ratings analyst Emir Mujkic. "Some insurers will have to adapt their business models, and others, particularly in the United Arab Emirates, will need to raise additional funds or look for alternative ways to comply with the new regulations. As insurers try to improve economies of scale, we may see some increased pressure on the industry to consolidate in 2018."

S&P Global Ratings anticipates that the insurance markets in the GCC will continue to grow and remain profitable overall in 2018. However, having been strong in the past few years, gross written premium growth is likely to be slower in some markets in 2018. Although longer-term growth prospects remain satisfactory, they will continue to depend heavily on economic growth and regulatory-driven initiatives, such as the implementation of new compulsory insurance covers.

There might be more volatility of profitability in 2018, as increasing operating costs and fierce competition in the GCC insurance sector will continue to put pressure on less-profitable companies.

"Since investment returns typically contribute to a significant share of earnings, geopolitical risks and fluctuations in global equity and commodity prices could lead to greater volatility in investment returns in 2018," said Mujkic. "We consider that these factors may therefore increase the gap between the large insurers, which are often more diversified and profitable, and their smaller counterparts."

Slow GDP growth, resulting from relatively low hydrocarbon prices and increasing geopolitical risks in 2017, has continued to affect the fiscal and economic performance of countries across the Gulf. As a result, “we lowered our ratings on Bahrain (B+/Stable), Oman (BB/Stable), and Qatar (AA-/Negative) in 2017. Changes in sovereign ratings during the year also had a knock-on effect on the ratings on a small number of insurers in Oman and Qatar. Despite higher oil prices and stronger forecast real GDP growth--ranging from 1.5% (Saudi Arabia) to 3.5% (Kuwait), compared with a range of -0.75% (Kuwait) to 2.5% (Qatar) in 2017 — we still forecast government budget deficits across the GCC in 2018. In addition, geopolitical risks and volatility in hydrocarbon prices will continue to affect GCC equity markets.

These factors, together with ongoing political risks, will continue to put pressure on economies in the region, the report said. “We also took negative rating actions in 2017 due to company-specific events, such as large accumulated losses from underwriting or investment activities, resulting in weaker capitalization levels. As in 2017, we believe that company-specific events or economic risks could negatively affect the credit conditions for insurers in 2018,” S&P said. — SG