RIYADH — The Saudi banking sector maintained a year-on-year growth in 2017 with 8.7 percent increase in net profit and 0.4 percent rise in total assets, KPMG’s said in its recently released version of the GCC listed banks results report.

The report titled “GCC Listed Bank Results: Shifting Horizons”, analyses the results of selected listed banks in GCC. It summarizes bank’s results against selected key performance indicators for the year ending Dec. 31, 2017 and compares these with the same information for the year ending Dec. 31, 2016.

For Saudi Arabia, the largest economy among the GCC member-countries, 2017 was widely considered to be a year of recovery and consolidation for its banking industry. Total listed banking sector assets have remained relatively stable year-on-year with a slight increase of 0.4 percent to $592.5 billion in 2017, according to a new KPMG report.

The report said the total assets for Saudi banks grew by 0.4 percent ($2.4 billion) in 2017 which happens to be one of the lowest asset growth rates for the country in recent years. The majority of the growth can be attributed to the growth in the Islamic banking assets, where both corporate and retail segments grew.

Profitability for the listed banks in 2017 increased by 8.7 percent, driven by a slight increase in the total asset base, an increase in the SIBOR rate during 2017 which improved margins, and a slight reduction in operating expenses. CIR, on average, improved by 2.0 percent industry-wide as a result of the increased margins. Net impairment charges increased by 3.5 percent, reflecting an improving market conditions, while bearing in mind certain legacy exposure issues which may still exist in the banks’ books.

The liquidity situation, on average, improved by 1.7 percent for the KSA banks in 2017, primarily due to an increase in deposits with relatively stable lending undertaken by the banks in 2017. “The corporate segment, due to being cautious, generally preferred to keep cash at banks as opposed to deploying it in the market,” the report noted.

Commenting on the report, Adrian Quinton, Head of Financial Services, KPMG in Saudi Arabia, said “in the light of the unique and impressive political and economic circumstances the region has witnessed (in 2017), reflects the resilience of the banking sector.”

He added the report “highlights the increased optimism on the back of these positive results which, coupled with the rising oil price environment, have resulted in banks shifting strategies from the more conservative approach witnessed in recent times, to a more innovative and growth-driven focus, albeit in a measured manner.”

He further said “last year, KPMG professionals made a number of predictions in areas such as tax, regulatory reform, customer focus, digitization, cost efficiencies, governance, and capital/fundraising. Many of these predictions came true in 2017, and continue to support our overall positive long-term outlook on the sector.”

The reforms undertaken by the GCC governments as well as other pump-priming activities bode well for both their economies as evidenced by the healthy results of the banking industry in 2017.

The report said that the region’s banking sector witnessed “robust asset and profitability growth, lower loan impairment and NPL ratios, increased cost efficiencies, and improved capital positions” last year.

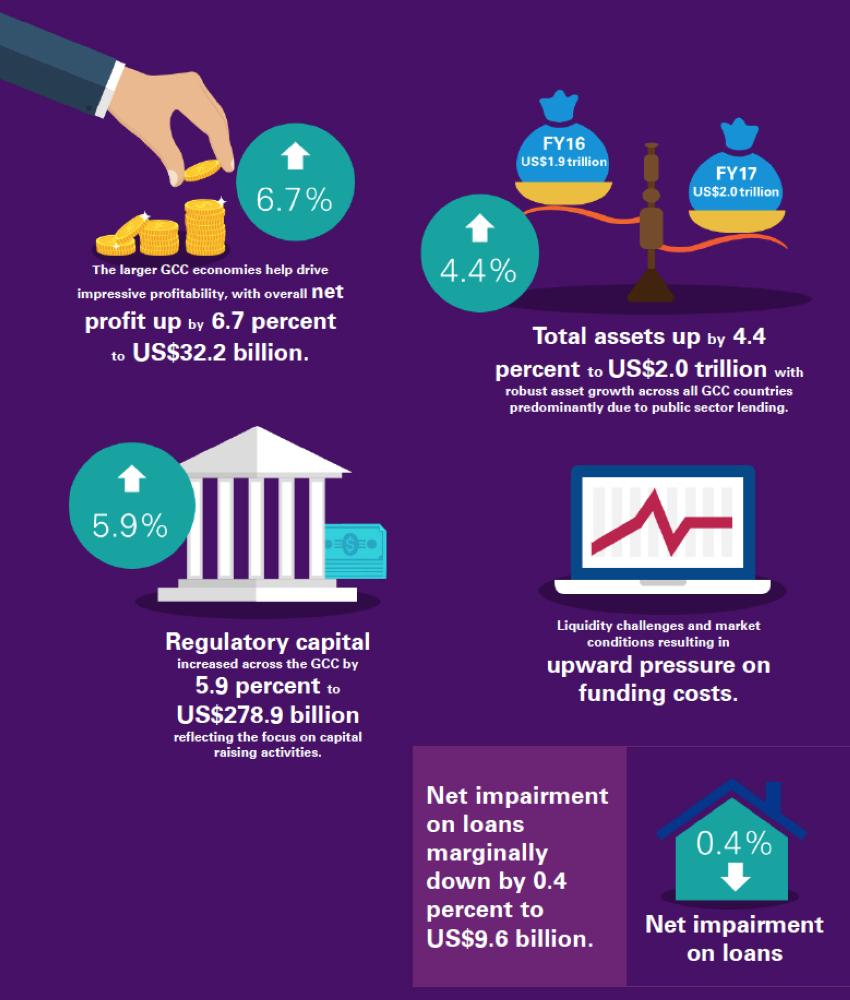

KPMG report noted that the larger GCC economies helped drive impressive profitability, with overall net profit up by 6.7 percent to $32.2 billion. Total assets rose by 4.4 percent to $2.0 trillion, with robust asset growth across all GCC countries predominantly due to public sector lending. Moreover, the report revealed that regulatory capital increased across the GCC by 5.9 percent to $278.9 billion reflecting the focus on capital raising activities.

Based on the imposing outcome, KPMG predicted that this year (2018), there would be “continued customer focus through innovation and technology, cost operational efficiency initiatives (will) remain a priority, expected rising provisions in an IFRS 9 environment, and increased capital and fundraising activity,” Quinton remarked.

The increase in the Interbank Offered Rate in 2017 had a positive impact on margins and resulted in increased profitability which, as a result, drove increased ROA and ROEs in 2017.

However, Saudi banks continued to face cost pressures as the general cost of doing business increased in 2017, despite the CIR across the banking industry slightly improving by 2.0 percent compared to the previous year. The introduction of expat levies, dependent visa fees and other government fees on employment have increased the cost of employment for banks.

During 2017, Saudi Arabian banks have invested in improving cost efficiencies through initiatives such as rationalizing their branches, optimizing system capabilities and refocusing on core products.

As of December 31, 2017, outstanding credit extended by banks totaled $61.0 billion, a rise of 6.4 percent over the level witnessed a year ago. During 2017, total deposits grew by over 5.6 percent to $56.1 billion to support the stability of the banks’ funding base.

Against this backdrop, increased opportunities and asset growth in the region were expected in 2018 owing to government reforms.

The positive momentum is expected to continue due to the strengthened contribution from the non-oil sector, especially infrastructure, leisure and tourism.

Most banks in Saudi Arabia are recognizing the need to embrace fintech and explore solutions such as blockchain for KYC, trade finance and general ledger purposes. “While no banks in Saudi Arabia have fully implemented such solutions as yet, we expect the banks to begin bucking this trend in 2018,” KPMG report noted.

The implementation of IFRS 9 from Jan. 1, 2018 was seen to impact on the banks’ capital. Accounting for IFRS 9 expected credit losses (ECL) is expected to increase credit loss provisions in the industry on average by 10 - 45.0 percent.

IFRS 9 will also strategically impact the banks in terms of how they assess risk appetite, pricing, credit sanctioning and credit stewardship of their businesses.

Nonetheless, new banking licenses are expected to be issued in 2018 to foreign financial institutions looking to establish and or expand their presence in Saudi Arabia. SAMA has issued new rules and regulations around banking licensing to support aspiring new entrants. International capital is expected to play a vital role in achieving Vision 2030.

Besides, the report projected banks to significantly invest in implementing pre and post attack controls to mitigate cyber security risks. Owing to the new AML rules and regulations coming into force in 2018, there will be ever more scrutiny placed on the bank’s anti-AML measures going forward.

In addition, KPMG report said allowing women to drive from June 2018 will significantly widen the consumer base for auto leasing, and public-private partnerships (PPPs) are expected to drive projects in 2018 within various sectors where private sector financing will be required.

The Aramco IPO is expected to take place by the end of 2018. “This capital amount is expected to be deployed in infrastructure, energy, real estate and education sectors to complete existing projects, but also to drive new ones which would boost balance sheet growth for the banks,” the report noted. — SG