IN Saudi Arabia rising demand for healthcare and government initiatives favoring increased private sector participation, look set to drive expansion in the sector and open new doors for investors. Saudi Arabia: Knight Frank, recently released a report discussing the healthcare sector in Saudi Arabia: ‘Healthcare in Saudi Arabia – Opportunities in the Sector – May 2018’

The key findings of the report are:

In the short to long term the healthcare space in Saudi Arabia presents itself as a sector with high growth opportunities. While, demand for healthcare in Saudi Arabia is set to continue growing. Key drivers include a demographic shift and an increase in health insurance coverage.

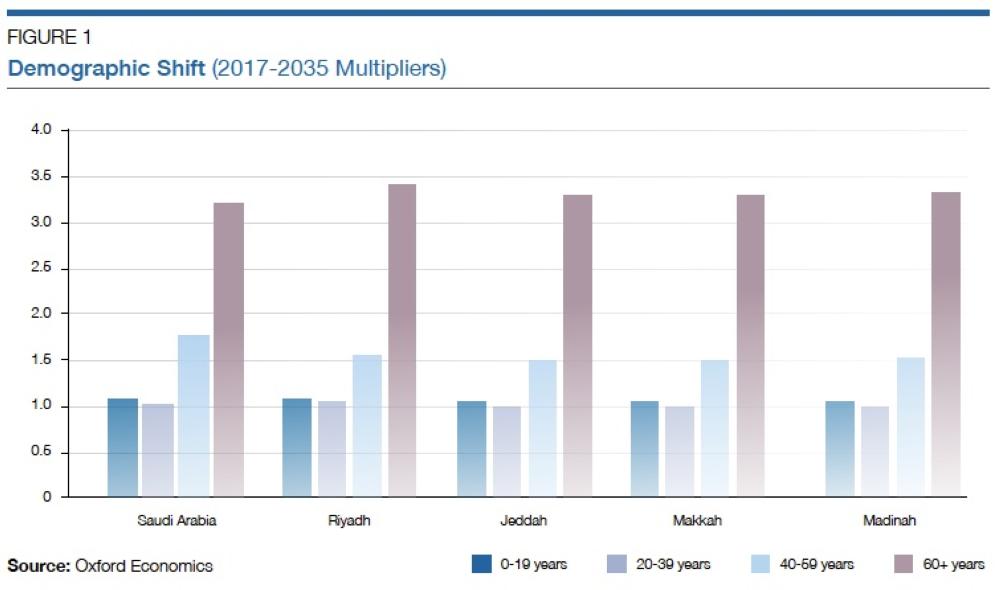

Population dynamics are forecast to shift, with population between the ages of 40 and 59 increasing by 1.5 times and population over the age of 60 increasing more than 3 times from 2017 to 2035. This will increase demand for health services and broaden the requirement for specialist care.

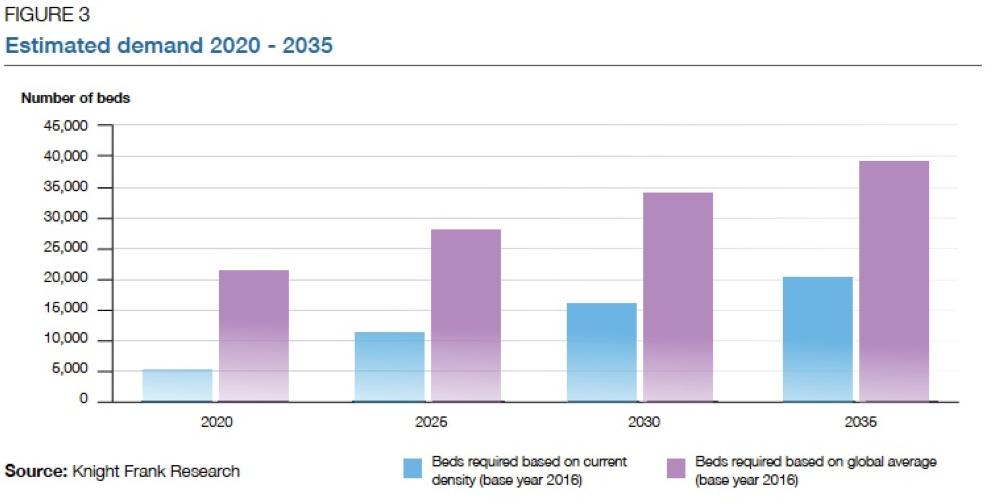

Forecasted demand gap due to population growth and facilities requirements, create a business case for the development of additional facilities in the country. Saudi Arabia requires an additional 20,000 hospital beds by 2035 (based on current density) to meet the expected population growth in the country.

The Kingdom’s National Transformation Plan (NTP) and privatization program have placed healthcare on a fast trajectory to privatization and growth over the coming years, offering number of opportunities to existing operators/ investors and new entrants.

From a value perspective, healthcare investments generate attractive yields. The yield range varies due to the risk/return profile of the investment i.e age of the asset, length of lease tenure, covenant strength, security and position of the operations on the business life cycle.

“Over the next decade, population dynamics are forecast to shift, with a significant increase in the population over 40,” noted Dr. Gireesh Kumar, senior manager, Healthcare, “This indicates an expected increase in the burden of lifestyle diseases and the associated co-morbidities which would trigger an upsurge in demand for highly specialised medical and surgical care in the Kingdom.”

Shehzad Jamal, partner, education and health, commented: “Healthcare is undergoing a transformation phase – long term view and thorough research must be taken while investing in the sector to ensure investments match current and forecasted demand.”

The excerpts of the report:

Investing in alternative real estate asset classes such as healthcare is a growing trend among global and local investors seeking diversification benefits as well as long term stability given the defensive nature of the underlying income stream. In Saudi Arabia, rising demand for healthcare and government initiatives favoring an increased participation from the private sector look set to drive expansion in the sector and open new doors for investors.

Taking a closer look at the Saudi Arabian healthcare market, we note that the prevailing picture is one that offers a number of opportunities to existing operators / investors and new entrants, hence the possibility to unlock a significant growth potential by fulfilling existing and future gaps. Saudi Arabia has a young population with approximately 70% below the age of 40 years, and health services have been planned based on this demographic profile. If we fast-forward to 2035, the population would still be considered young, despite a significant change in healthcare demand dynamics:

• Population between the ages of 40 and 59 will increase by 1.5 times in Saudi Arabia.

• Population over the age of 60 is forecast to increase by more than 3 times in Saudi Arabia.

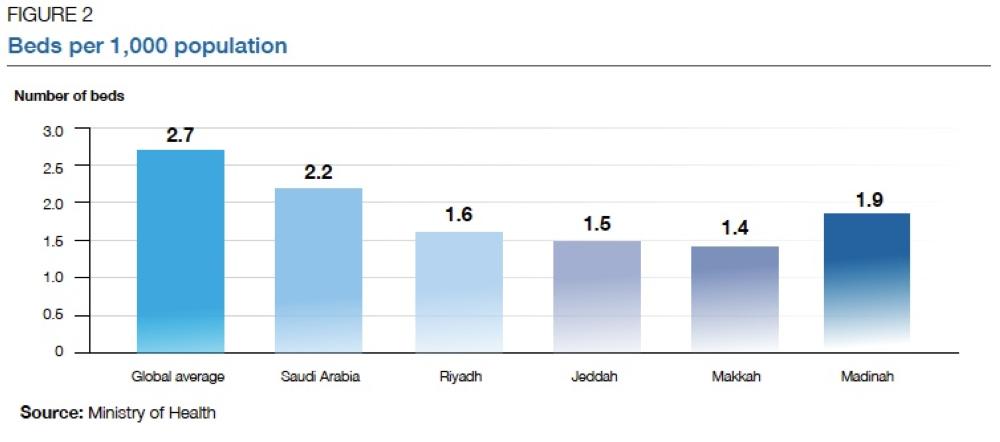

Healthcare facilities in the holy and economic cities are lower than the national average and significantly lower than the global average. These facts create a business case for the establishment of healthcare facilities.

• Economic cities – these cities generally have better healthcare infrastructure than the rest of the country and host patients from the other parts of the Kingdom. Lower infrastructure density and the existing strain on healthcare resources presents opportunities for additional beds, centers of excellences, specialized and niche healthcare services commonly found in developed metropolises. Careful study of specialization opportunities and their subsequent introduction will help improve availability of healthcare in the country, curb outbound medical tourism and save outflows from the exchequer.

• Holy cities – private healthcare facilities in these cities can be classified as basic with potential for upgrade. With the relaxation of visa requirements, these cities should strongly consider the introduction of medical tourism to complement their religious tourism. Over the last ten years, the number of Haj pilgrims remained within the region of 1.9 million to 3.2 million, while Umrah pilgrims peaked in 2017 at 8.4 million. Assuming adequate infrastructure is in place, these cities are uniquely positioned to cater to the spiritual and medical requirements of the population. This would appeal to a significant number of Muslims who would consider benefiting from spirituality and holiness of these cities whilst being treated.

Forecasted demand

• To keep pace with population growth, Saudi Arabia would require an additional 5,000 beds by 2020 and 20,000 beds by 2035, based on the current density of beds.

• Based on the global average of bed density, Saudi Arabia was faced with a gap of 14,000 beds in 2016 and this gap is expected to widen to 40,000 beds by 2035.

Government initiatives

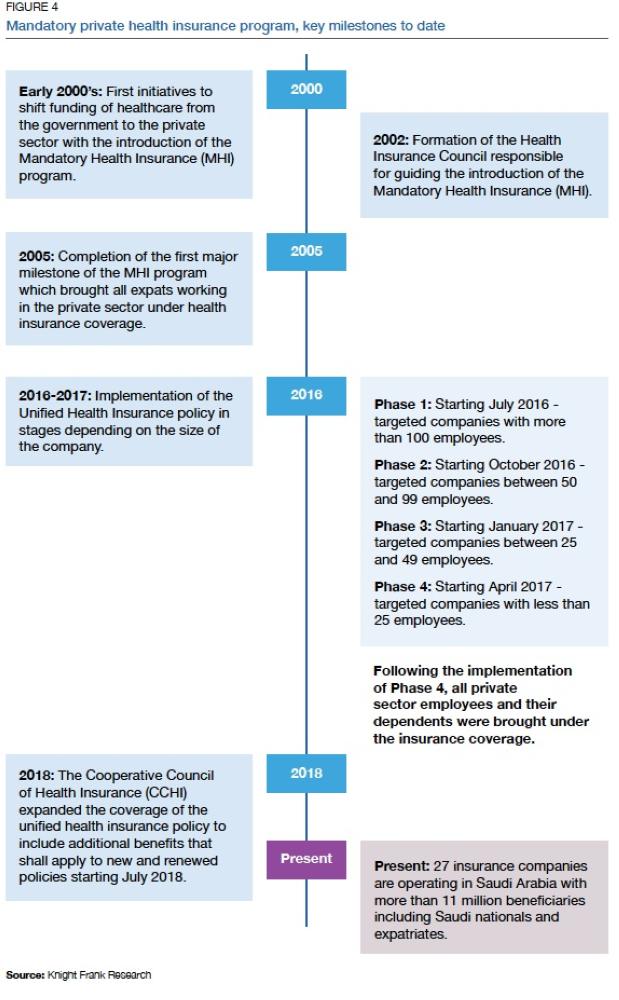

Several government-driven initiatives are changing the dynamics of the sector and contributing in reshaping the healthcare landscape in the Kingdom by creating a stronger institutional set-up and effective regulatory frameworks to promote private sector investment in healthcare.

Early 2000’s: First initiatives to shift funding of healthcare from the government to the private sector with the introduction of the Mandatory Health Insurance (MHI) program.

2002: Formation of the Health Insurance Council responsible for guiding the introduction of the Mandatory Health Insurance (MHI).

2005: Completion of the first major milestone of the MHI program which brought all expats working in the private sector under health insurance coverage.

2016-2017: Implementation of the Unified Health Insurance policy in stages depending on the size of the company. 2018: The Cooperative Council of Health Insurance (CCHI) expanded the coverage of the unified health insurance policy to include additional benefits that shall apply to new and renewed policies starting July 2018.

Present: 27 insurance companies are operating in Saudi Arabia with more than 11 million beneficiaries including Saudi nationals and expatriates.

Phase 1: Starting July 2016 - targeted companies with more than 100 employees.

Phase 2: Starting October 2016 - targeted companies between 50 and 99 employees.

Phase 3: Starting January 2017 - targeted companies between 25 and 49 employees.

Phase 4: Starting April 2017 - targeted companies with less than 25 employees.

Following the implementation of Phase 4, all private sector employees and their dependents were brought under the insurance coverage.

Mandatory Health Insurance

The rollout of the Mandatory Health Insurance (MHI) to private sector employees in Saudi Arabia took place in various stages.

Saudi Vision 2030 and the NTP

Healthcare is one of the main focus areas of the Vision 2030 and the National Transformation Plan (NTP). The main goal of the Saudi Vision 2030 is to diversify the economy away from hydrocarbons and trigger a greater participation of the private sector by encouraging both local and international investments in a number of key sectors, one of which is healthcare.

Privatization of government services is expected to help meet the goals set out in Vision 2030 with the aim to increase private sector’s contribution to GDP from 40% to 65% in 2030. The NTP, which was developed to help fulfill the Saudi Vision 2030, has identified number of key targets to be met by each government body by 2020. The Kingdom’s healthcare plan under the NTP has placed the sector on a fast trajectory to privatization and growth over the coming years.

Targets set out by the NTP for the Ministry of Health for the year 2020 include:

• Increasing private healthcare expenditure from 25% to 35% of total healthcare expenditure.

• Increasing the number of licensed medical facilities from 40 to 100.

• Increasing the number of internationally accredited hospitals.

• Doubling the number of primary healthcare visits per capita from two to four.

• Decreasing the percentage of smoking and obesity incidence by 2% and 1% from baseline respectively.

• Doubling the percentage of patients who receive healthcare after critical care and long-term hospitalization within 4 weeks from 25% to 50%.

• Focusing on improving the quality of preventive and therapeutic healthcare services.

• Increasing focus on digital healthcare innovations.

In parallel with a shift towards a greater participation of the private sector, healthcare is expected to remain a key area of government spending in this transition phase. The allocated budget for healthcare under the NTP stands at SR23 billion, of the total SR268 billion (over 5 years ending 2020) which is the fourth largest area of spending under the NTP.

We see this as an encouraging step for the sector amidst the ongoing transformation. From a public finance perspective, healthcare remains the third largest area of government spending following military and education, accounting for 15% of total expenditures in the 2018 announced budget.

Privatization and PPP schemes

Privatization is seen as a key focus area in the Saudi Vision 2030 and the NTP. The strategic objectives stated for healthcare in the NTP include:

• Privatization of one of the medical cities through a Public-Private Partnership (PPP) scheme.

• Increasing private sector share of spending in healthcare through alternative financing methods and service providers.

In April 2018, Saudi Arabia announced an ambitious privatization plan, which includes 14 PPP investments to be completed across 10 sectors including healthcare by 2020.

The key targets of the privatization plan in relation to healthcare include:

• Updating and expanding primary care across Saudi Arabia.

• Providing additional rehabilitation and long-term care beds across the Kingdom through the creation of PPP structures.

• Planning for the establishment of additional medical cities.

• Preparing King Faisal Specialist Hospital & Research Center for privatisation and help it in achieving its leadership position through focusing on innovation.

• Updating and expanding laboratory and radiology services across the country in partnership with the private sector. The most significant constraint to the development of the PPP market in Saudi Arabia is the absence of a clear legal framework for investors. In February 2018, Custodian of the Two Holy Mosques King Salman approved a number of decisions taken by the Saudi Health Council including the establishment of a PPP program in the healthcare sector.

Value perspective — healthcare real estate

The investment and potential returns that can be generated from healthcare assets is evident. The data on builtup-area (BUA) and construction costs are sourced from industry averages and can vary due to the type of offering and speciality. The yield sits on a range based on risk profile, which increase or decrease based on the factors mentioned below:

• Age of the asset

• Length of the lease tenure

• Covenant strength and security

• Position of the operations on the business life cycle

In the short to medium term, based on the factors mentioned above, the healthcare space in Saudi Arabia presents itself as a sector with high growth opportunities. To ensure long-term success it is important to carefully study the market, identify gaps and be willing to continuously embrace technological advancement.

Private investment in healthcare is being guided by the Saudi Arabian General Investment Authority (SAGIA) and we can expect to see further changes to regulatory controls in order to achieve the goal of increased private sector involvement and investment while ensuring a suitable regulatory framework for the upcoming privatization waves and PPP schemes within the healthcare sector.