JEDDAH — The Islamic Corporation for the Development of the Private Sector (ICD, Aa3 stable) benefits from a robust capital position and strong liquidity, although its weak asset quality remains a challenge, says Moody's Investors Service in an annual report.

Thaddeus Best, an analyst at Moody's, and co-author of the report titled "Islamic Corporation for the Development of the Private Sector - Aa3 stable Annual Credit Analysis," said "the ability, and willingness of the ICD's main shareholders to provide support are also credit strengths, demonstrated by strong participation in the second general capital increase to date."

The ICD's main shareholder, the Islamic Development Bank (IsDB, Aaa stable), continues to support the

corporation's credit profile, even as its shareholding is slowly diluted through capital increases.

As with many multi-lateral development banks (MDBs), the ICD maintains high levels of liquidity to compensate for the lack of recourse to emergency funding such as central bank liquidity. ICD's debt service coverage ratio remains strong at 15.4% in 2017, and it maintains a minimum of one year's net cash requirements under stressed conditions, assuming no market assess.

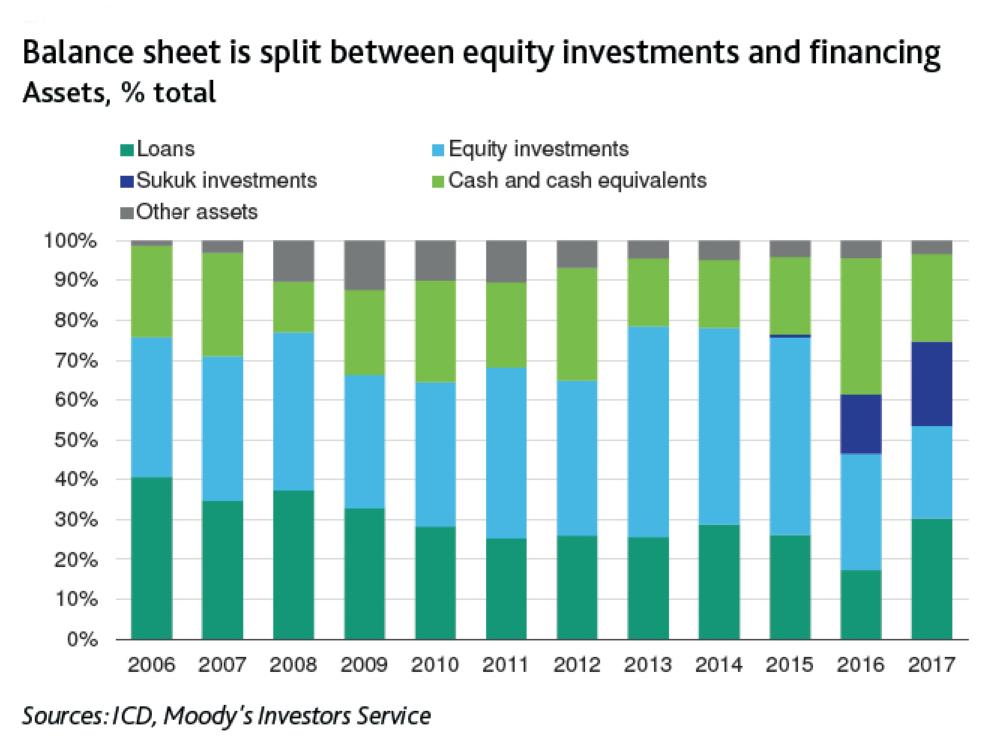

MDBs that focus on the private sector tend to have riskier operating profiles than other MDBs and equity

investments can be more volatile than lending. Due to these two features, the ICD has a structurally weaker

asset quality profile than other MDBs, as evidenced by the large losses sustained in 2017 arising from

revaluations in the equity portfolio, and the history of high non-performing loans.

Meanwhile, the ICD's credit challenges include its weak asset quality, as reflected in the term finance portfolio's track record of high nonperforming loans (NPLs) and only slow improvements over time. The absence of contractual callable capital also sets the ICD apart from other, higher-rated MDBs.

The rating outlook is stable. NPLs will remain elevated alongside the strong balance sheet expansion and as the corporation continues to invest in the relatively risky private sectors of emerging and frontier markets. This is balanced by strong liquidity underpinned by further sukuk issuances, and the capacity of shareholders to provide support. As would a sustainable improvement in the Corporation's asset quality track record, with NPLs ranging well below 10% of total loans and a higher credit quality in the treasury.

Downward rating pressure could result from weaker shareholder support, whether measured by the credit rating of key shareholders or resources made

available by shareholders during general capital increases. A sharp increase in leverage beyond medium-term plans or a further deterioration of asset quality would likely result in a lower rating and equity portfolios. — SG