NEW YORK — The outlook for the global refining and marketing sector over the next 12 to 18 months has been changed to positive from stable, Moody's Investors Service said Saturday in a new report.

The key drivers of the outlook change are expected EBITDA growth of 13%-15% through 2019 and likely into 2020 due to higher distillate margins and favorable crude differentials, while gasoline inventories will remain elevated despite high demand through next year.

"Over the next 12 to 18 months, distillate margins and favorable crude differentials will propel crack spreads, a crucial factor in oil refiners' profitability," said Arvinder Saluja, a Moody's VP and senior

analyst.

"Meanwhile, gasoline demand will remain high, though demand from OECD countries likely will decline over the longer term due to increasing

vehicle fuel efficiency and biofuel consumption," he added.

Globally, distillate fundamentals will remain more favorable than gasoline fundamentals, with higher demand from the industrial, mining and construction sectors, and already low inventories. Distillate prices

are less elastic than those for gasoline, while new international maritime emission standards will mandate low-sulfur fuels for the shipping industry, sparking demand for compliant products in an already

tight market.

Meanwhile, for many North American refiners, domestic crudes will remain cheaper. Distillate demand will remain robust, with below-average

inventories due to strong economic growth and potential regulation. Even so, a sudden drop in demand for gasoline, or production surpassing

demand, would increase risk.

The Annual World Refining Outlook 2018 report said despite the recent OPEC and non-OPEC production agreements, “we continue to forecast a low price oil environment for the foreseeable future. Consequently, we expect products demand to be robust, especially for light distillates (naphtha and gasoline) but also for middle distillates too.”

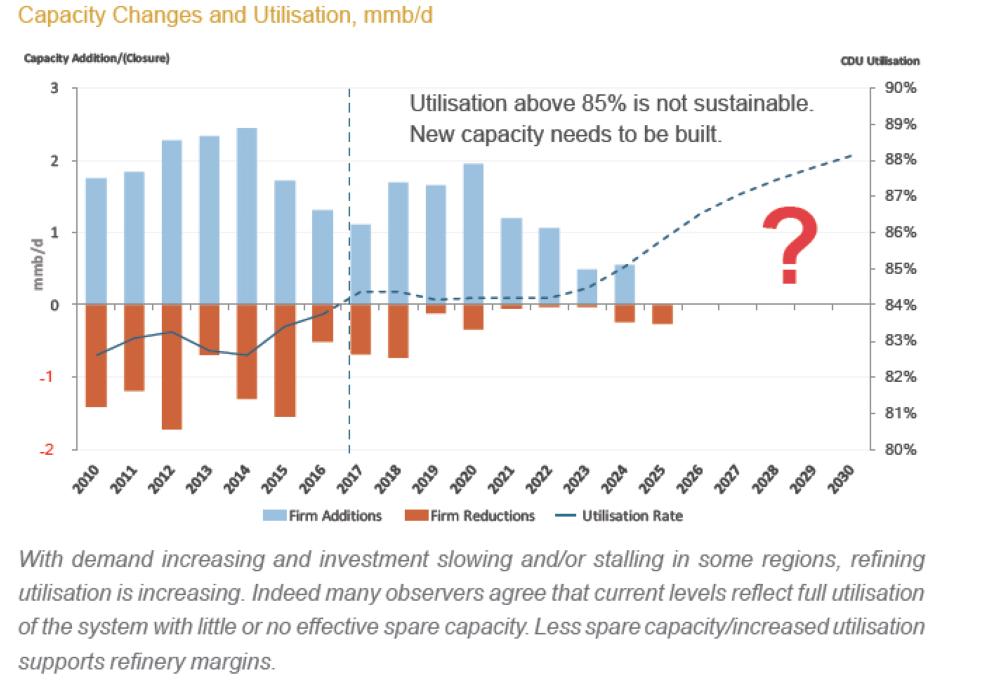

At the same time, CAPEX for investment in any part of the oil business will be limited, with refining investment continuing to be under pressure. While there are many projects announced in the

press, only a small percentage are actually built. the report noted.

Consequently, the pressure on existing capacity and what is actually built is increasing. There is plenty of potential for the strong cracks and margins seen over the last 2 years or more to continue.

In this study we look at this potential, what the main

Refiners are continuing to invest in sophisticated upgrading capacity, essentially converting fuel oil into gasoline and distillate. Recent and imminent new capacity has focused on distillate production in particular, it addeqd.

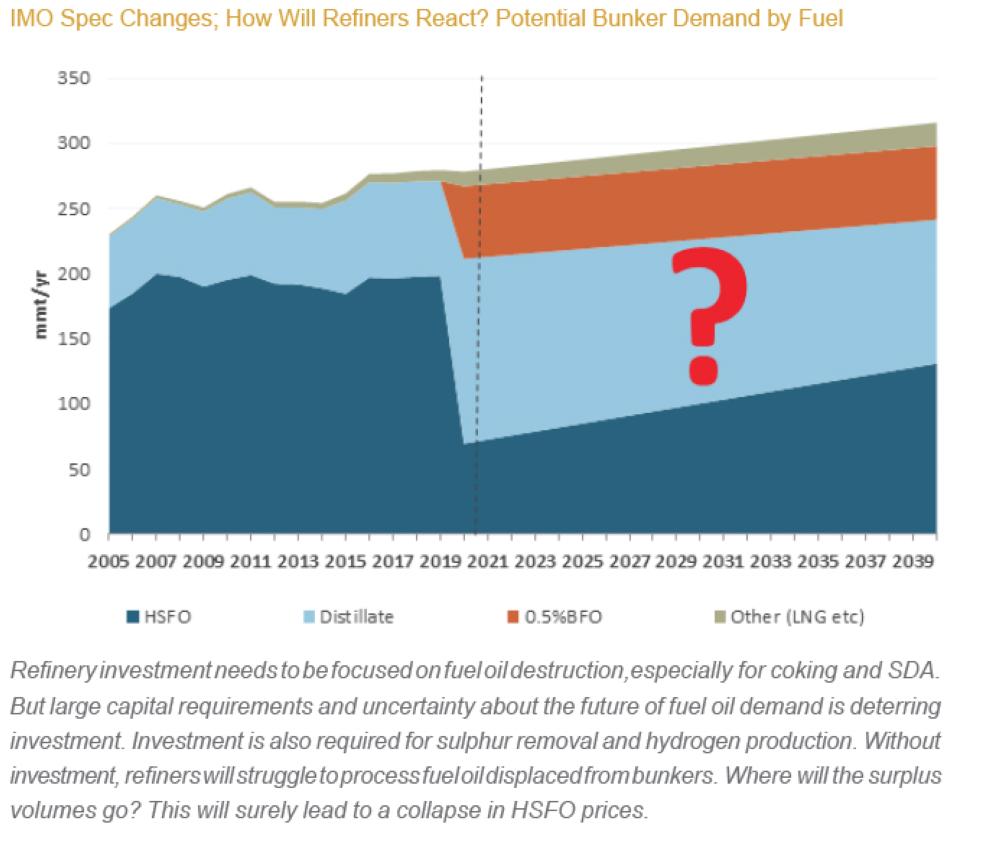

The report forecast that by 2020, “will see the biggest change ever to the demand barrel with the introduction of new specifications for bunker fuel oil (to 0.5% S max without flue gas mitigation) for the world’s marine fleet. We look at how refiners and the fleet will react to this, the implications for distillate and fuel oil demand and balances, product cracks and refinery margins.” — SG