JEDDAH — Tightening liquidity conditions worldwide, high geopolitical risks in the Middle East, and challenges inherent to sukuk issuance will likely dampen sukuk market performance in 2019. S&P Global Ratings forecast.

S&P anticipates total issuance of $105 billion-$115 billion ($28 billion-$32 billion for foreign currency issuances and $85 billion-$95 billion excluding reopening of instruments) this year.

Nevertheless, S&P expect higher demand for funding in most GCC countries, given “our reduced oil price assumptions compared with last year›s outturn of $71 for Brent.

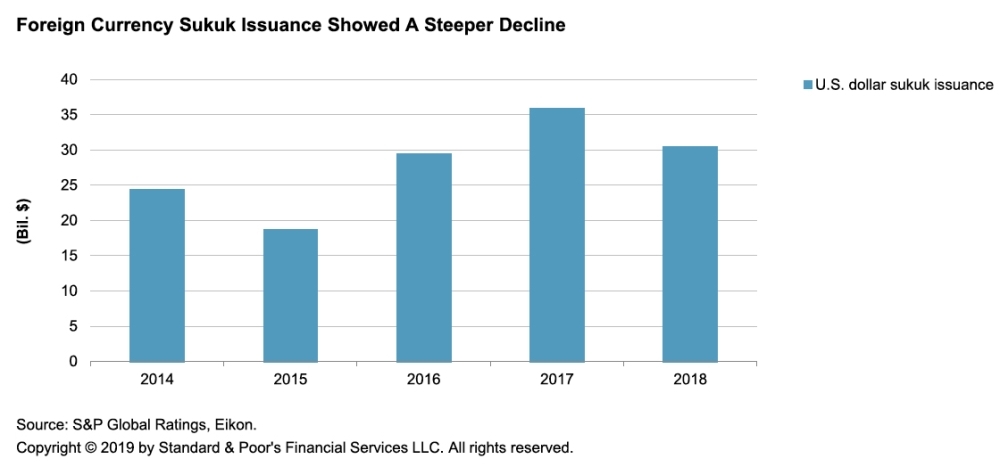

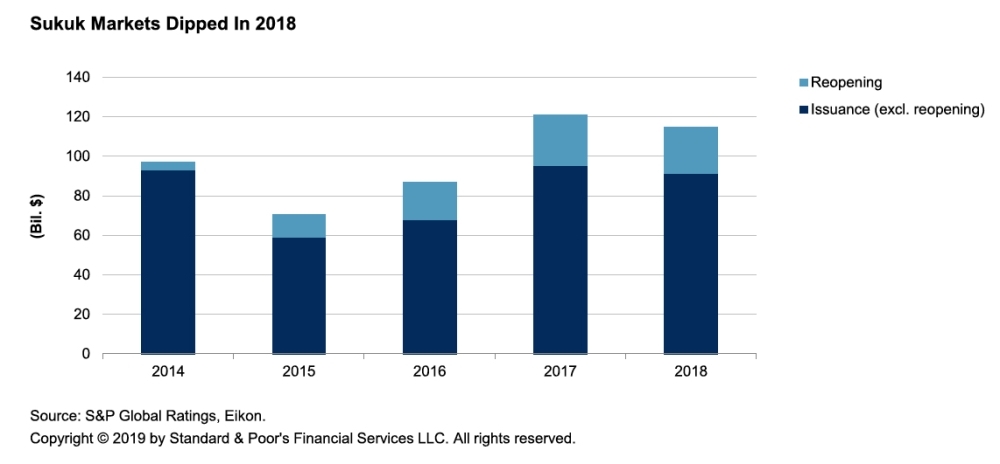

“We also expect Malaysia will continue to support market growth. Last year, new sukuk issuance totaled around $91.4 billion ($114.8 billion including reopening, which consists of issuances under local currency unlimited programs) compared with $95.7 billion in 2017 ($120.6 billion with reopening). The decrease was even more visible, at 15.1%, for foreign currency sukuk issuance, primarily in US dollars. The marked drop in issuance in Saudi Arabia and Qatar were partly offset by issuances from the Central Bank of Kuwait and a hike in private-sector issuances in the United Arab Emirates (UAE). Activity in Malaysia and to a lesser extent Indonesia continued to support the market, contributing collectively to around 52% of new issuance in 2018. Issuers in Turkey also stepped up their issuances to diversify their investor bases amid substantial reliance on external debt and reduced access to global capital markets in the second half of the year.

Sukuk issuances from Kuwait, the UAE, and Turkey helped the market avoid a steeper decline last year, in our view. For example, Kuwait›s central bank started to offer sukuk as liquidity management instruments for domestic Islamic banks. And, in the UAE, private-sector issuers frontloaded some of their issuances to face upcoming maturities, in anticipation of less supportive market conditions. However, we see several reasons why overall issuance volume could be subdued this year (The numbers in the charts could differ slightly from our previous publications, due to exchange rate movements):

European and US-based investors generally account for around one-quarter to one-third of sukuk holders. We expect that, as in 2018, major central banks will continue to close the liquidity tap this year, albeit gradually, leaving investors with less funding to invest in sukuk. Overall, we think issuers› cost of funding will keep rising, and liquidity from developed markets channeled to the sukuk market will continue to reduce and become more expensive. Investors are also concerned about the economic cycle after a long period of expansion. At some point, the cycle will turn and investors will become more risk averse.

Moreover, liquidity conditions in the GCC improved in 2018, but appear uncertain in 2019. “We assume oil prices will remain flat at $55 in 2019 and beyond. We base our Sukuk issuance forecasts on these assumptions. However, oil prices can be extremely volatile and represent upside and downside risks to our forecast.”

The trend of reopening Sukuk supports our base-case forecasts. These are issuances under unlimited local currency programs, which were reserved to a few Asian countries in the past. From 2018, Saudi Arabia not only joined this category of issuers but also raised $11.3 billion under this scheme.

Heightening geopolitical tensions in the region came back on investors› radar over the past 18 months. It started with the boycott of Qatar in early June 2017 by a group of Arab states, which, in our view, has reduced the cohesiveness of the GCC countries and complicated policy predictability. Developments in Saudi Arabia have also attracted investors› attention. What›s more, the reinstatement of US sanctions on Iran and continued animosity between Iran and some of its GCC neighbors are not helping investors› perception of risks. The potential de-escalation of hostilities in some countries in the region could help reduce concerns over the next 12 months. Oil prices will continue to drive much of the GCC›s financing needs

We expect the Brent oil price to average $55 per barrel in 2019. Financing needs in the GCC are likely to increase this year, given that the oil price is lower than last year. However, many private-sector issuers in the GCC issued sukuk in 2018 to prefinance upcoming maturities and prepare for more stressed capital market environments. Moreover, the complexity related to sukuk issuance might push some issuers to relegate sukuk issuance to second place. Overall, the volume of issuances from the GCC is likely to be flat.

Sukuk standard-setting bodies agreed in the last quarter of 2018 to work together to devise a smoother issuance process. While this is a significant development, realizing this goal is still far off. Ideally, the process for sukuk issuance should be as easy as that for issuing a conventional bond. Standard legal documents and standard Sharia rulings, allowing the issuer to plug in an underlying asset and tap the market, should become the norm, in our view. Today, and for the foreseeable future, the sukuk issuance process remains more complex than for conventional bonds, where issuers need to go through several additional steps such as identifying an underlying asset, choosing the best suitable structure, and putting together lengthy legal documents.

What happened with Dana Gas acted as a wake-up call for investors and put the standardization debate back at the top of the agenda for standard setters and policymakers. Dana Gas reportedly defaulted on its sukuk, alleging a lack of Sharia compliance, which triggered lawsuits in the U.K. (the court rulings were in favor of sukuk holders) and in Sharjah. In the end, holders of Dana Gas› sukuk decided to settle with Dana Gas rather than try to enforce the U.K. judgment in Sharjah. Among other things, the Dana Gas case illustrates the potential issues that arise when trying to enforce foreign judgments in local jurisdictions, especially when Sharia is the ultimate source of the law. We think the standard setters will keep that in mind as they strive toward greater standardization.

We recognize, however, that the Islamic finance market has achieved a certain level of standardization for the most common structures, while a few new instruments still need some refinements. In particular, investors are asking for additional clarity on the risks attached to the Murabaha-Mudaraba structure that is widely used in some jurisdictions.

In our view, standardization for cross-border sukuk issuance is not only achievable, but will also boost issuance volumes. It will restore the attractiveness of the instrument to issuers through a smoother, faster issuance process and increased clarity on the underlying risks for investors. The use of fintech could also support this agenda. Blockchain and smart contracts could improve the traceability of cash flows and assets. Smart contracts could facilitate out-of-court resolution in a pre-agreed way from the onset of the transaction.

This idea is not new. The absence of broad and deep capital markets in the GCC is a weakness, and some authorities have started to tackle it. The UAE is an example where the authorities have brought together capital market participants to come up with a plan to develop a broad local-currency sukuk market. In our opinion, the recipe for success consists of greater standardization for Sharia interpretation and legal documents (possibly endorsed by a regulator) that offers incentives to sukuk issuers. In Malaysia, for example, issuers benefit from tax relief if they choose the sukuk route. In the absence of corporate income tax in UAE, the authorities could envisage other types of incentives, such as requiring Islamic financing for specific government projects or waiving other government levies if the financing instrument is Sukuk. The authorities have also started to address the challenge of standardization requiring the adoption of AAOIFI›s sharia standards and establishing a high sharia authority. Coming up with a set of capital-market-authority preapproved legal documents could be the next step. — SG