JEDDAH — Like their conventional peers, Islamic banks in Gulf Cooperation Council (GCC) countries have seen growth slow in recent years. Some banks' exposure to Turkey has exacerbated the situation, after the country experienced significant volatility in 2018, and this remains a major source of risk, S&P Global Ratings said last May 6.

In its report, S&P said though that despite this and challenges at home, several GCC Islamic banks maintained sound asset-quality and profitability indicators. In addition, their funding profiles remain healthy, dominated by core customer deposits, and capitalization is still a major positive rating factor.

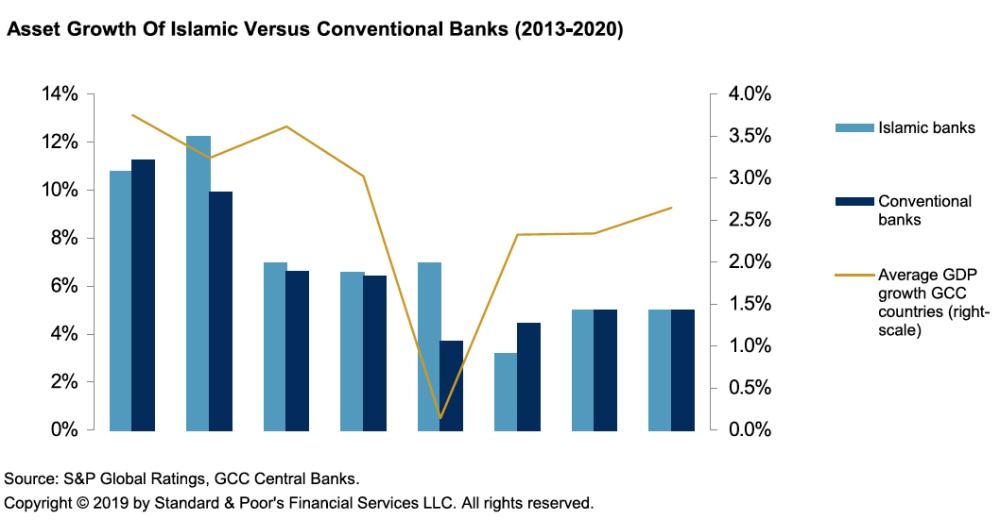

In 2018, GCC Islamic banks expanded slower than conventional peers for the first time in five years, attributed to three main reasons:

• Some of the Islamic banks we analyzed were hit by currency depreciation (particularly of the Turkish lira), which reduced their asset base in US dollar terms.

• Certain banks in the United Arab Emirates (UAE) recorded strong growth, but they represent only a small proportion of our Islamic banks sample, compared with the conventional one.

• Islamic banks in Qatar displayed a negative growth rate for 2018 due to consolidation and the slowdown of some economic sectors in the country.

However, the growth difference was a mere 1%, which explained why the conventional and Islamic banks will see similar growth patterns in 2019-2020.

The report saw mid-single-digit growth for both types of banks due to several factors. These include S&P forecast of muted GCC economic growth over this period, despite some benefit from government spending and strategic initiatives such as national transformation plans, the 2022 FIFA World Cup, and Dubai Expo 2020. We also assume that oil prices will average $60 per barrel (/bbl) in 2019 and 2020, pushing governments and the private sector to adopt a more careful approach to spending.

"We view the recent oil recovery as somewhat fragile and note that forward curves indicate market expectations of lower prices in the future. Furthermore, S&P expected geopolitical risk to remain high, with pressure on some strategic sectors such as real estate in the UAE and Qatar. “We think lower oil prices and geopolitical risk, combined with a few pressure points stemming from the global economy, will continue to weigh on consumer sentiment, prompting lower spending – especially if financed with debt.”

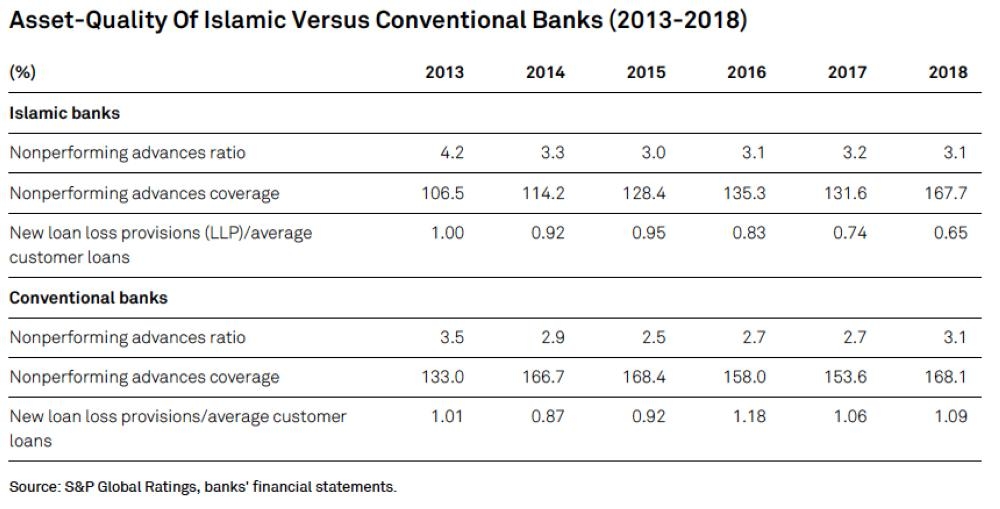

GCC Islamic banks' asset-quality indicators stabilized in 2018, with the nonperforming financing ratio averaging 3.1% of total financings for the banks in our sample. Provisions more than covered these exposures with a coverage ratio of 167.7% on the same date. This was an improvement over 2017 thanks to the adoption of International Financial Reporting Standards (IFRS) 9 or Financial Accounting Standard (FAS) 30 for banks reporting under Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) standards.

Also, last year, Islamic banks' asset quality indicators did not deteriorate as did those of conventional banks, which saw their nonperforming loan (NPL) ratio increase to 3.1% on average from 2.7% at end-2017. “We attribute this development to the clean-up and write-off operations of some Islamic banks in our sample, rather than a genuine improvement in asset quality.

“We think that Islamic banks' asset quality should be similar, if not slightly weaker than that of conventional banks in the GCC. This is because both bank types are comparable, with businesses primarily comprising the collection of deposits and extending of finance to the real economy in their countries,” S&P said.

Furthermore, Islamic banks tend to have higher exposure to the real estate sector due to the asset-backing principle inherent to Islamic finance.

S&P also noted that Islamic banks cannot charge late payment fees, unless they are donated to charities at the end of the exercise, meaning that clients tend to prioritize payments on conventional rather than Islamic exposures.

However, with the transition to IFRS9/FAS 30, Islamic and conventional banks will even more closely align.

At end-2018, the average Stage 2 exposure for Islamic banks in our sample reached 10% of total exposure. This number is just indicative as it includes an estimation of Stage 2 exposure for Kuwaiti Islamic banks, which are yet to publish their numbers. The amount of Stage 2 financing to total financing was 11.2% at end-2018 excluding our

estimates for Kuwait.

“We expect problematic assets to stabilize at about 15% of total assets in the next 12-24 months, with some transitions between Stage 2 and Stage 3 given the pressure on the real estate and contracting sector in some countries,” the report said.

Another trend is the significant increase in Islamic banks' coverage ratios at end-2018, coupled with a stable cost of risk (excluding outliers) that is lower than conventional banks. Banks have taken the opportunity of IFRS 9 transition to set aside as many provisions as they can, given that the opening impact is charged to equity and not to income. — SG