JEDDAH — A further escalation in geopolitical tensions could provide additional short-term upside to oil and gold prices, a report report prepared by three analysts from UBS AG and UBS said.

That being said, “in our base case we still target a Brent oil price drop to $60/bbl during 1H20. Gold, on the other hand, is expected to reach $1,600/oz. Negative real rates in the US and a weaker US dollar favor stronger precious metal prices in general,” analysts Dominic Schnider, CFA, CAIA; Giovanni Staunovo; and Wayne Gordon said.

Following the US airstrike in Iraq, crude oil and gold moved higher during Friday trade. Crude oil prices are up nearly 4% to $68.7/bbl for Brent and $63.4/bbl for WTI and 1.3% to nearly $1,550/oz for gold, respectively, at the time of writing. The precious metal complex (silver, platinum and palladium) tends to benefit from bouts of market uncertainty. Industrial metals, on the other hand, are down in line with risk assets, with equities and growth- sensitive currencies coming under pressure.

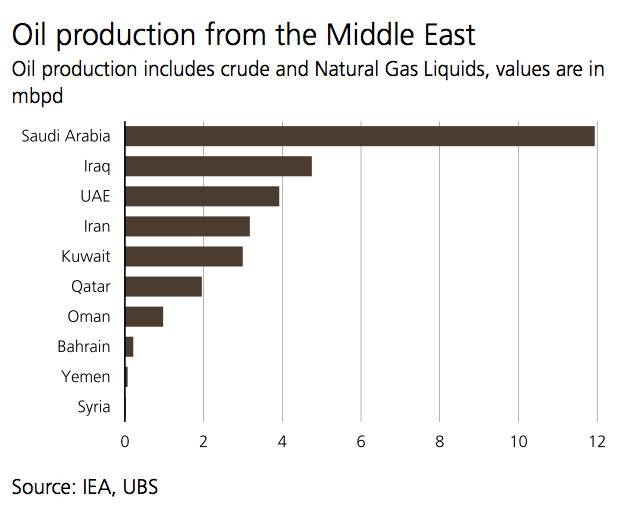

They said a more serious escalation in the Middle East, “which is not our base case, would have a broader economic and financial market impact through sharply higher crude oil prices.” The region accounts for almost one third of global oil supply. Iran and Iraq produced 2.13 million barrels per day (mbpd) and 4.65mpbd of crude in November 2019, respectively, and combined accounted for nearly 8% of global oil liquids supply in November 2019, including natural gas liquids production of 1.15mbpd.

Market participants are concerned that the tensions between Iran and the US could impact the political stability of Iraq and the oil production in the second largest OPEC producer.

While a number of US oil workers have been evacuated from the Iraqi oil fields near Basra, the Iraqi oil ministry has highlighted that production and exports have so far not been affected.

While neither the US nor Iran wish for an escalation in tensions, no one knows if, when, and how Iran will respond, the analysts said.

Considering these risks, markets have added a risk premium on fears tensions could escalate. US Secretary of State of Mike Pompeo stated that the US remain committed to de-escalation and does not seek war with Iran but will not stand by and see American lives put at risk.

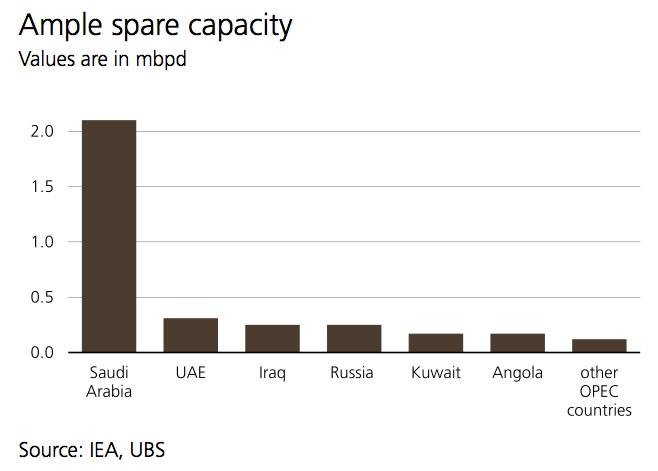

Any larger sustained disruption to supply could send prices toward $75/bbl or higher. But adequate-to-ample crude spare capacity (OPEC's and Russia's spare capacity is around 3.3mbpd, while the return of production from the Neutral Zone shared between Saudi Arabian and Kuwait could increase that spare capacity by another 0.3mbpd over the next 6-12months), in addition to strategic oil reserves held by OECD countries, provide a key supply cushion.

Moreover, on the back of non-OPEC supply growth driven by the US and Norway outpacing modest oil demand growth this year, we still expect an oversupplied oil market in 2020 (0.3mbpd), particularly in 1H20. Hence, we believe Brent price moves above $70/bbl are unlikely to be sustained over several months. “This was the case in September when Saudi oil processing facilities were damaged and prices reversed fully within two weeks. We therefore reiterate our bearish price guidance for Brent, and see oil declining toward $60/bbl during 1H20, with risks skewed to the upside,” the analysts said.

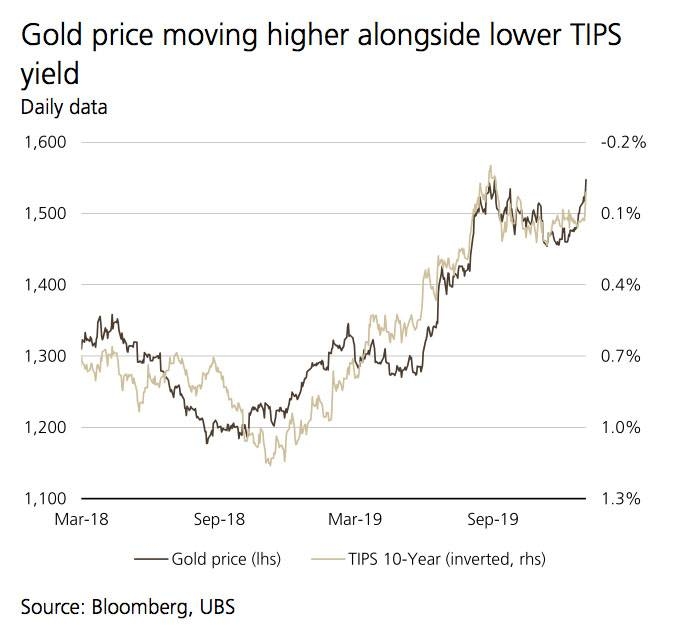

Given heightened geopolitical tension in the Middle East, all precious metal prices shifted firmly higher on Friday. Given its safe-haven status, gold advanced the most within the precious metals complex. Geopolitical tension in the Middle East has the potential to support even higher prices in the very short run. However, the impact usually fades over a longer period of time. So it's possible that some of the gains will be priced out in the latter part of 1Q20. But that doesn’t mean investors should turn negative on precious metals, especially gold.

“We continue to target a gold price move to $1,600/oz in 2020. The underlying drivers are not Middle East market uncertainty, rather they are increasingly-negative US real interest rates and the broad-based weakening of the US dollar. A renewed rise in the Federal Reserve's balance sheet and the risk of more Fed rate cuts to support a slowing US economy tend to be supportive of precious metals. This holds particularly true in a world where interest rates are expected to stay low for longer and with rates in many economies near zero or negative. Thus, we see value in staying long the metal from a thematic angle and the value in the diversification benefits the metal brings to equity oriented investor.

With risk assets coming under pressure, particularly equities, industrial metal prices are down up to 3.5% at the time of writing. “We still believe any bigger setback in base metal prices, i.e., in the mid-single digits or more – should be used to build some long exposure. This stance largely hinges on our view that global capex will recover this year and that economic growth in Asia will not be affected by the developments in the Middle East.”

In short, growth in Asia should still accelerate this year. In China, which is a major consumer of base metals, housing activity is expected to hold up in 1H20, and infrastructure investment and industrial production activity should gain greater traction. The resulting pick-up in industrial metal demand, particularly from 2Q20 onwards, holds the key to another round of lower visible inventories, the analysts opined.

“Even if market deficits narrow in 2020, we believe the supply side has sufficient pricing power to command higher prices for several reasons: a) inventory levels stand at low, or very low, levels; b) compared to 2019, demand should accelerate next year; c) higher production costs could be an issue as the global economy reflates; d) the lack of capex investments in recent years makes the supply side more vulnerable; and e) we target a broadly weaker US dollar. So, for now, we like to sell the downside risks in nickel and lead for a premium. We like strike levels at $13,100 for nickel and $1,800/ mt for lead, and target maturities of six months. Pullbacks in copper below $6,000/mt should be used to build longs.” — SG