GCC banks achieve 6% profit growth in 2017

04 Apr 2018

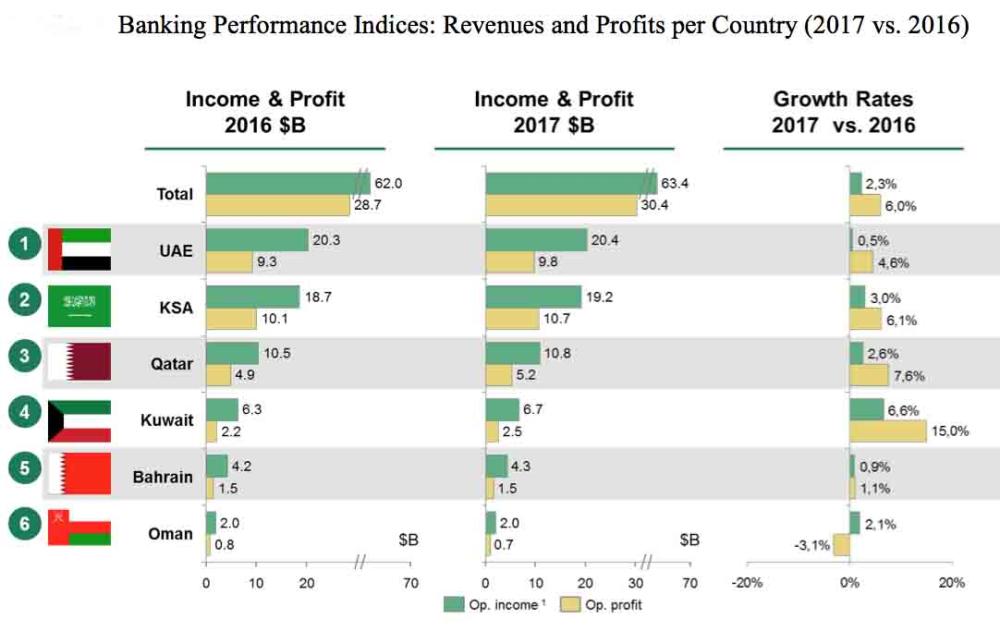

JEDDAH — Despite low revenue growth of 2.3 % in 2017 from about 3 percentage points in 2016, GCC banks achieved 6% profit growth due to declining LLPs and cost reductions, BCG’s annual banking performance study revealed.

GCC banks are adapting well to a slowing revenue growth regime and profits climbed more than twice as strong through reduced loan loss provisions as well as tight cost management,” said Dr. Reinhold Leichtfuss, Senior Partner & Managing Director at BCG's Middle East office.

The main customer segments – retail and corporate banking – grew revenues at rates of 3 percent and 5.4 percent, respectively.

Despite this moderate growth, the index of GCC banks still exceeds that of their international counterparts, which, however, saw stronger growth in 2017.

The lower rate in 2017 stemming almost exclusively from major customer segments such as retail and corporate banking. This implies a significant decline in revenue growth rates for four years in a row in most countries.

The upside is that banks were still able to grow profits with a rate more than twice as high as revenues and also that loan loss provisions (LLPs) were reduced once again. Moreover, most banks managed to reduce their operating expenses, leading to a cost reduction of 1 percent on aggregate for the large GCC banks.

Based on the banks’ 2017 annual results released in the first quarter of 2018, the latest study is part of BCG’s annual banking performance indices, which measure the development of banking revenues (operating income) and profits for leading GCC banks.

BCG launched the first edition of the banking performance index in the GCC in April 2009, creating a customized index specifically for the regional banking markets. The index covers the largest banks in Bahrain, Kuwait, Qatar, Oman, Saudi Arabia, and in the UAE.

“The 2017 BCG Banking Performance Index includes 44 banks from across the GCC, capturing about 80 percent of the total regional banking sector,” added Peter Vayanos, successor of Dr. Leichtfuss as head of the Financial Institutions practice for BCG ME.

International banks saw strong top line growth close to 5 percent in 2017 and an even stronger recovery in profits in 2017; however, remain far behind GCC banks regarding the index level.

Banks in most countries see stronger growth in profits than in revenues.

In 2017, Kuwait banks led the pack in terms of growth figures, with 6.6 percent in revenues and 15 percent in profits. While in 2016 many banks across all countries in the GCC experienced a negative development in profits, in 2017, the vast majority of banks grew profits stronger than revenues except for Oman. “This is a pattern we have been seeing in more mature banking markets, such as in Europe or the US, for a number of years,” said Vayanos “The two largest markets, UAE and Saudi Arabia, are naturally closer to the average, with UAE still close to zero revenue growth the second year in a row. The positive message is the healthy profit growth of UAE banks, at 4.6 percent,” said Dr Leichtfuss. “The revenue growth stagnation stems from a tighter risk appetite as well as portfolio optimization initiatives of banks which seek to enhance risk-adjusted returns.”

As for LLPs, 2017 showed healthy improvement of 2.7 percent in contrast to 2016, when LLPs had catapulted upwards. UAE and Oman experienced the strongest declines of 8.4 and 16.5 percent respectively, followed by Saudi Arabia with 6.5 percent.

Moreover, operating expenses were well controlled in the GCC countries. Even the UAE banks reduced this figure by 2.7 percent in total, led by the country’s largest banks, and Qatar banks by 6 percent while Saudi Arabia banks managed to keep costs constant. All countries remained significantly below the long-term cost CAGR of ~11 percent.

In 2016, GCC banks concluded a three-year decline in growth, down from a high level in 2014. In the long term, however, GCC banks experienced a halving of overall growth rates. In 2017, Kuwait was the only country in which the growth rate bounced back from low level.

In 2017, retail banking growth shows strongly diverging trends across the GCC countries around the average of 3 percent revenue growth and 14 percent profit growth. Retail banking in Saudi Arabia grew revenues by 7 percent and profits by 24 percent, while UAE banks in total saw a decline in retail revenues by 2 percent but a profit growth of 15 percent. Qatar banks achieved a revenue growth of 12 percent but experienced a sharp profit decline of 22 percent. Bahrain banks had to accept a decline of 3 percent in both retail revenues and retail profits.

Corporate banking revenues grew moderately by 5 percent while profits only increased by 3 percent.

Saudi Arabia and Qatar saw strong corporate banking revenue growth around 7 to 8 percent, and achieved good profit growth as well. UAE banks again saw stronger growth in profits than in revenues. Kuwait takes a significant drop in profits owing to a strong increase in LLPs.

Superiority of strategies, business models and execution are decisive for long term performance of GCC banks.

“In 2017, only 18 percent of GCC banks were able to achieve double digit revenue growth, while twice as many experienced double digit profit growth. The positive profit trend is reflected in that only 7 percent of banks saw negative profit growth. The number of banks in 'group' and for the 'retail' and 'corporate' segments deviate, since not all banks have a complete segment reporting yet,” said Vayanos. “According to BCG’s analysis, it is clear that banks with superior strategies and strong business models can truly execute decisively and achieve the strongest growth.”

Over the past decade, the region’s leading banks have grown at double or triple the rate of its average banks. In almost all cases, such a development is based on a superior and consistently-executed strategy.

“In the coming three to five years, we consider the digitization of processes as the most important task that banks need to achieve; this will enable advanced banks to achieve the next level of customer experience as well as cost efficiency. Moreover, particularly in the banking sector, new business opportunities are perpetually arising in the wake of the continued digital transformation, noted Dr. Leichtfuss. — SG