JEDDAH — S&P Global Ratings believes sovereign borrowing in the Middle East and North African (MENA) could decrease by 6% this year after falling 30% in 2017. This is chiefly because fiscal consolidation measures in all Gulf Cooperation Council(GCC) countries and higher oil prices will likely reduce GCC sovereigns' funding needs. In its report, S&P forecast that the 13 MENA sovereigns we rate will borrow about $181 billion this year from domestic and international commercial sources, down $11 billion from 2017.

The decline will result from fiscal consolidation measures across the Gulf Cooperation Council and the uptick in oil prices, which will likely push down net-oil-exporting governments' financing needs.

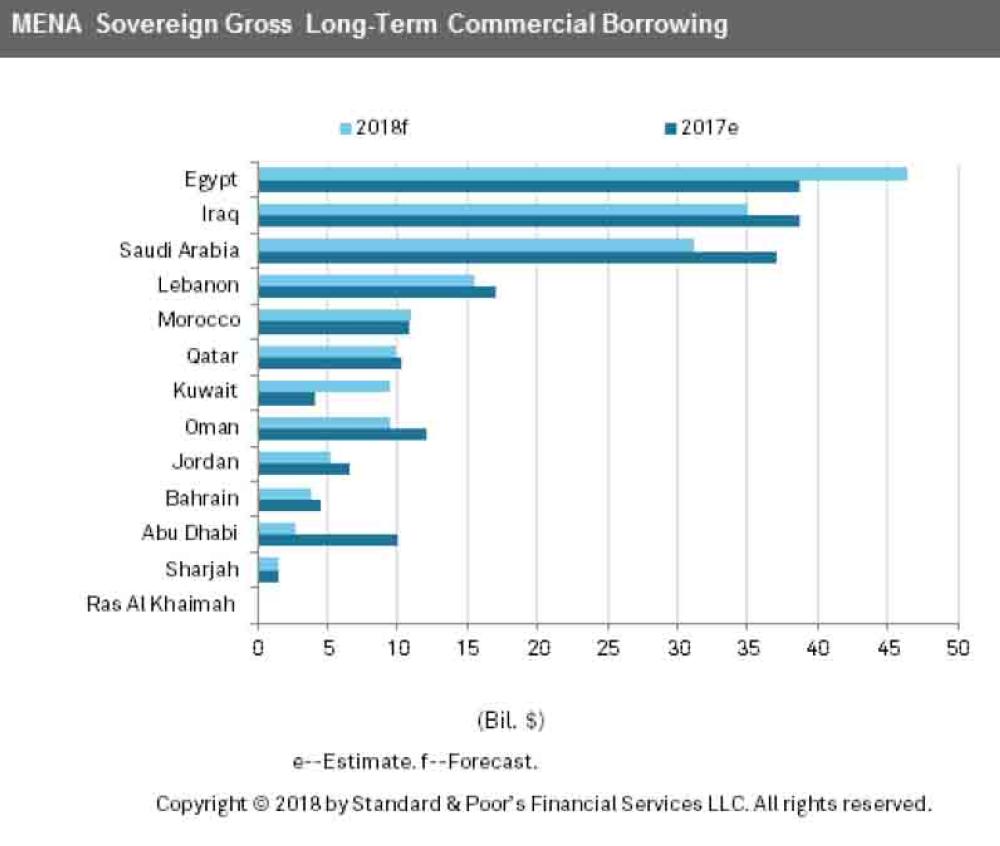

Egypt remains the largest borrower with $46.4 billion, or 26% of the region's gross commercial long-term borrowing, followed by Iraq ($35 billion or 19% of the total) and Saudi Arabia ($31 billion or 17%).

S&P exceeded MENA sovereigns' absolute commercial debt will increase by $21 billion to about $764 billion at year-end 2018, up 3% from 2017.

We expect that about 40% of MENA sovereigns' $181 million of gross borrowing this year will go toward refinancing maturing long-term debt, resulting in an estimated net borrowing requirement of $108 billion (see tables 1 and 2). Adding amounts owed to bi- and multilateral institutions, total debt will reach about $860 billion, a year-on-year increase of $13 billion, or 2%. However, the share of non-commercial official debt is set to decline to 11% of total sovereign debt as of year-end 2018, from 12% in 2017. We expect that outstanding short-term commercial debt (original tenor of less than one year) will fall to $131 billion by the end of this year.

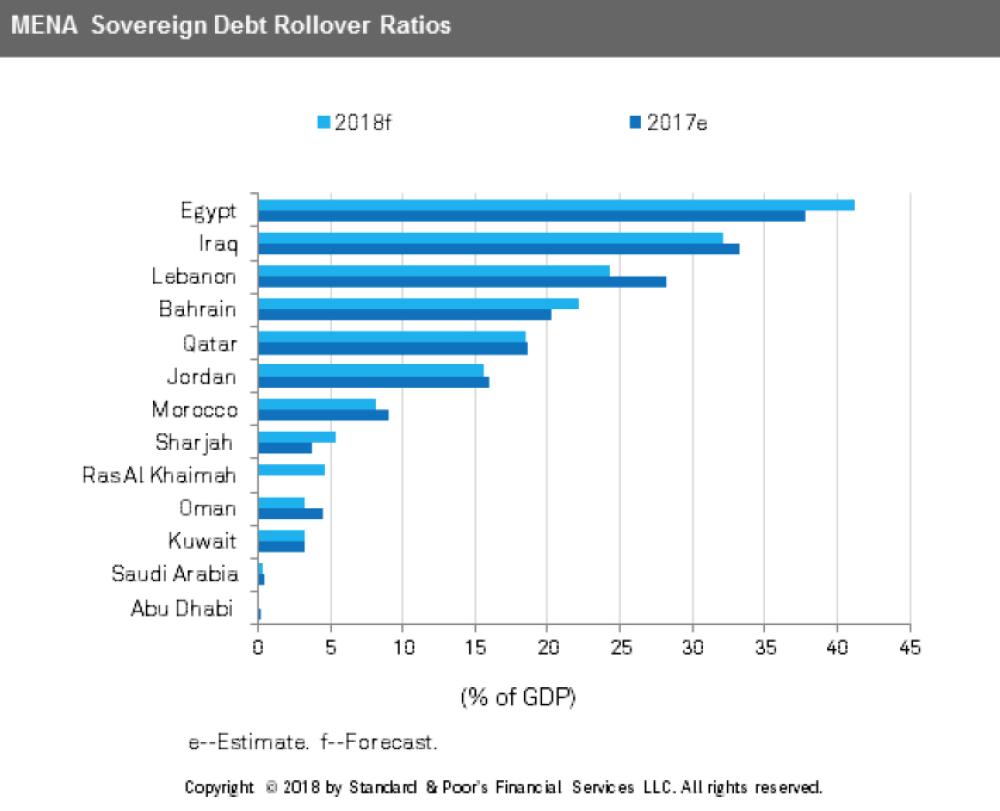

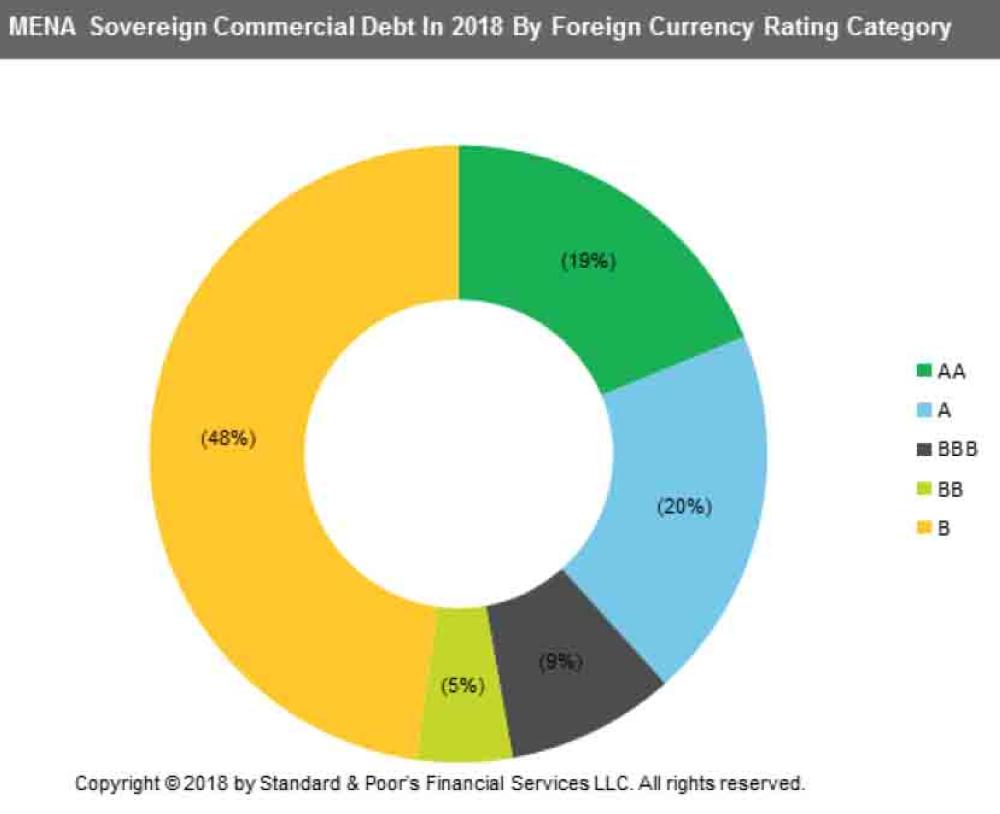

For 2018, we project that sovereigns' commercial debt rated in the 'AA' category (Abu Dhabi, Kuwait, and Qatar) will be 19% of the total, up from 16% in our 2017 report. The share of 'A' category debt (Ras Al Khaimah and Saudi Arabia) will rise to about 20%. No MENA sovereigns are rated 'AAA'. Due to the rise in the share of debt issuance by higher-rated MENA sovereigns, the share of commercial debt rated in the 'BBB' category or lower should fall to about 62% of the total from 67% at the time of our 2017 report. Egypt accounts for 19% of the total commercial debt we expect the region's sovereigns will issue by the end of 2018, with Lebanon at about 11%, closely followed by Iraq at around 10%. We calculate that Egypt will face the highest debt-rollover ratio (including short-term debt) in the region, reaching 41% of GDP, followed by Iraq (32%) and Lebanon (24%; see table 4 and chart 3). The rollover ratios of sovereigns with higher proportions of official debt tend to be lower because official debt typically has longer tenors than commercial debt. Our borrowing estimates for the 13 MENA sovereigns we rate (see table 5) focus on debt issued by a central government in its own name. We exclude local government and social security debt, as well as the debt of other public bodies and government-guaranteed obligations. In terms of commercial debt instruments, our long-term borrowing estimates include bonds maturing beyond one year, issued in the capital markets or as private placements, as well as commercial bank loans. Some of the estimates we use in this report, in addition to commercial debt, include official debt. We exclude government debt that central banks may issue for monetary policy purposes in some countries. All reported forecast figures are our own estimates and do not necessarily reflect the issuers' projections. Our estimates also reflect our expectations regarding central government deficits, our assessment of governments' potential extra-budgetary funding needs, and our estimates of debt maturities in 2018. Estimates that we express in dollars are subject to exchange rate variations. We expect Egypt, Iraq, and Saudi Arabia will issue the lion's share of commercial government debt in the region in 2018 (respectively 26%, 19%, and 17%). These three sovereigns' debt issuance will account for about $113 billion, or 62% of the total (see chart 1 and table 2). We expect Iraq will continue to have the largest share of bi- and multilateral debt in 2018 (40% of the total), with the next largest recipient of official funding being Jordan (18%). Of the 13 rated MENA sovereigns, seven are net hydrocarbon exporters. Morocco, Egypt, Jordan, Lebanon, and the emirates of Sharjah and Ras Al Khaimah are net hydrocarbon importers. Sharp oil price declines in 2014 and 2015 resulted in a significant widening of GCC fiscal deficits. In recent years, GCC sovereigns have implemented fiscal consolidation measures to cut government spending and increase non-oil government revenues. We expect regional fiscal deficits to moderate as a result, while the modest recovery in oil price of late should boost government revenues (see "S&P Global Ratings Raises 2018 Brent And WTI Oil Price Assumptions," published Jan. 18, 2018.

We expect GCC sovereigns' gross commercial long-term borrowing will total $68 billion in 2018, down from $80 billion in 2017. Regarding GCC central governments' deficit-financing strategies, Qatar, Bahrain, and Oman have largely focused on debt issuance rather than asset drawdowns; while Abu Dhabi, Kuwait, and Saudi Arabia show a more equal split between issuing debt and liquidating part of their assets. We note that most GCC countries have been tapping international debt markets in recent years to diversify their funding sources and reduce liquidity pressures in the domestic banking systems. — SG