THE Middle East hospitality market witnessed a steady growth in occupancy during the first quarter of 2018, according to the latest EY Middle East Hotel Benchmark Survey Report. Except for Jeddah, Beirut, and Doha, hotel occupancy across the MENA region saw an increase when compared to the first quarter of 2017. This increase was primarily due to a number of shopping festivals, improving bilateral relations, and overall pleasant climate conditions across the region.

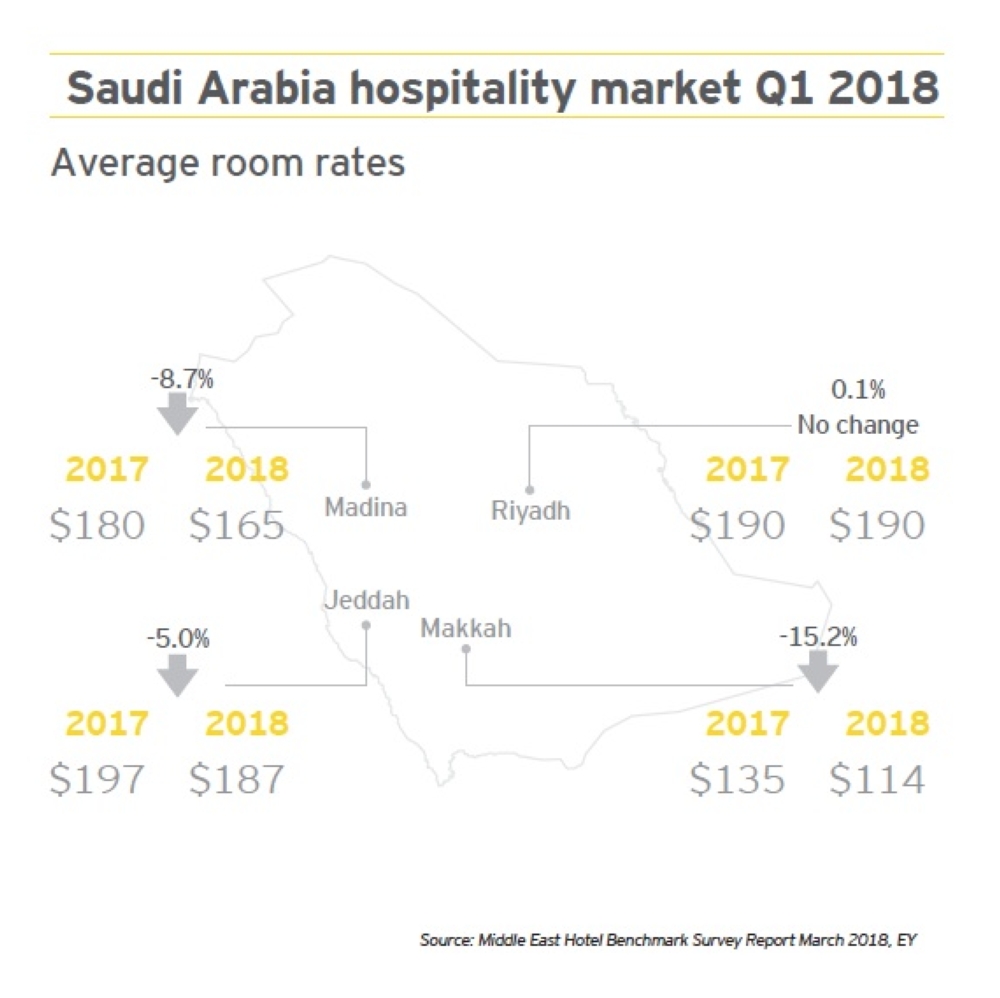

In Saudi Arabia, Madinah, Riyadh and Makkah witnessed an increase in occupancy; however, Jeddah witnessed a decrease of 5.7% points from 54.4% in Q1 2017 to 48.7% in Q1 2018. The hospitality market in Jeddah also witnessed a decrease in ADR by 5% from $197 in Q1 2017 to $187 in the same period of this year. This led to a decline in RevPAR by 15% from $107 to $91 in Q1 2018. The drop in KPIs in the Jeddah market could be attributed to an oversupply of hotels in the market along with softer macro-economic conditions.

Makkah witnessed a 2.8% point increase in occupancy from 61.5% in Q1 2017 to 64.3% in Q1 2018. However, the ADR decreased by 15.2% to $114 in Q1 2018 compared to $135 in the same period last year, which then resulted in a decrease in RevPAR by 11.4% from $83 in Q1 2017 to $74 in Q1 2018.

The Riyadh hospitality market witnessed growth across all KPIs with its occupancy increasing by 3.9% points from 57% in Q1 2018 to 60.9% in the same period this year. The ADR saw a marginal increase of 0.1%, which resulted in an increase in RevPAR from $108 in Q1 2017 to $116 in Q1 2018.

The Madinah hospitality market witnessed a 6.8% increase in occupancy from 64.5% in Q1 2017 to 71.4% in Q1 2018. The ADR decreased by 8.7% from $180 in Q1 2017 to $165 in Q1 2018. However, there was an increase in RevPAR in the market from $116 in Q1 2017 to $117 in Q1 2018.

Top MENA hospitality performer

In the first quarter of 2018, Dubai achieved the highest occupancy, average room rate (ADR) and RevPAR across the MENA region. The city’s occupancy reached 86.9% with an ADR of $293, which led to an overall RevPAR of $255 in Q1 2018.

Occupancy increases across GCC markets

In the United Arab Emirates, the hospitality market saw a slight increase in occupancy in Q1 2018 over Q1 2017. Occupancy in Dubai increased by 0.8% points from 86.1% in Q1 2017 to 86.9% in Q1 2018, possibly due to international visitors of the 23rd edition of the Dubai Shopping Festival as well the favorable weather. Even though there was a slight decline in ADR by 1.2% from $297 in Q1 2017 to $293 in Q1 2018, Dubai achieved the highest RevPAR in the region at $255 in Q1 2018, the same as last year.

Driving the overall hospitality KPIs for Dubai were the hotels located on the beach, which saw an increase across occupancy, average room rate and RevPAR in Q1 2018. In the first quarter of this year, the occupancy of beachfront hotels in Dubai reached 82.7% with an average room rate of $559, leading to a RevPAR of $462. Meanwhile, hotels in the city of Dubai saw a slight increase in occupancy with 88.7%, but RevPAR fell by 6.2% to $168 in Q1 2018 due to a 6.8% decline in the average room rate.

The hospitality market in Abu Dhabi also registered an increase in occupancy by 7.3% points, up from 79.3% in Q1 2017 to 86.6% in Q1 2018. The increase in occupancy may be attributed to the marketing efforts by Abu Dhabi’s Department of Culture and Tourism to engage more visitors from various Asian countries. However, the ADR decreased by 14.7% from $122 in Q1 2017 to $104 over the same period, leading to a decrease in RevPAR by 6.9% from $97 in Q1 2017 to $90 in Q1 2018.

Ras Al Khaimah saw an increase in occupancy by 4.5% points from 75.3% in Q1 2017 to 79.8% in Q1 2018. The hospitality market also witnessed an increase in ADR by 5.4% to $174 in Q1 2018 when compared to $165 in Q1 2017, which resulted in an increase in RevPAR by 11.6% in Q1 2018.

In Bahrain, the Manama market saw a 10.6% points increase in occupancy to 59.7% in Q1 2018 from 49.1% in Q1 2017. However, the ADR decreased by 6.2% from $187 in 2017 to $176 in Q1 2018. Yet the market still saw a growth in RevPAR by 14.1% from $92 in Q1 2017 to $105 in Q1 2018. The increased occupancy in Q1 can be attributed to the Bahrain Shopping Festival, which attracted around 122,000 visitors to the country.

The Kuwait hospitality market saw a 2.5% points increase in occupancy from 65.1% in Q1 2017 to 67.5% in Q1 2018. The market also witnessed a 4.5% increase in ADR from $191 in Q1 2017 to $200 in Q1 2018. These contributed to the overall increase in RevPAR by 8.5% from $124 in Q1 2017 to $135 in Q1 2018. This may be attributed to several events that drew regional visitors such as the Kuwait Motor Show, Kuwait Expo, and the Hala February Festival.

In Oman, the Muscat hospitality market also registered an increase across all KPIs. Occupancy increased by 1.1% points from 83.3% in Q1 2017 to 84.4% in Q1 2018 and ADR witnessed a 3.9% increase from $169 in Q1 2017 to $175 in the same period of this year. This led to an overall increase in RevPAR by 5.3% from $141 in Q1 2017 to $148 in Q1 2018.

Yousef Wahbah, MENA Real Estate, Hospitality and Construction Sector Leader, said, “The performance across the MENA region in Q1 2018 saw a steady growth influenced by positive factors such as countries like the UAE, KSA and Bahrain improving their international trade relations. The growth in occupancy rate was consistent throughout the first quarter, which shows a healthy traction of visitors to the region, many of whom most likely wanted to enjoy the pleasant weather conditions before the summer heat sets in. As events wind down in the second quarter of the year because of the start of the holy month of Ramadan and the summer season, we can expect a decline in occupancy across most of the GCC hospitality markets. However, cities such as Cairo, Amman and Beirut are popular tourism destinations among both Arab expats and Westerners alike, and are likely to see an uptick in occupancy, and subsequently RevPAR, across their hospitality markets over the summer.” — SG