JEDDAH — Banks in the Gulf Cooperation Council (GCC) should continue to breathe a little easier in the year ahead, S&P Global Ratings said in its Industry Credit Outlook released Monday.

The report said “2019 should mark a stabilization of GCC banks› financial profiles, following three years of significant pressure. What›s more, with the transition to IFRS 9, GCC banks have now recognized most of the impact of the softer economic cycle on their asset quality. We therefore believe that the amount of problematic assets, which we define as IFRS 9 Stage 2 and 3 loans, will likely remain stable, but do not exclude transition between the two categories.”

“We expect GCC economies to show stronger economic growth in 2019 of about 2.8% (unweighted average of Saudi Arabia, Kuwait, the United Arab Emirates, Qatar, Bahrain, and Oman). However, this growth will still be below the triple-digit oil-price era growth of 2011-2013. We therefore expect lending growth to remain at around the mid-single digits. At the same time, we think that cost of risk will stabilize at around 1.0%-1.5% of total loans. Thanks to IFRS 9, the buffer of provisions that GCC banks accumulated over the past years is now stronger. The new reporting standard, adopted from the start of this year, required banks to set aside provisions in advance, based on their loss expectations.”

Moreover, the report noted that “finally, we think that GCC banks› profitability will stabilize. It will benefit from the higher interest rates and the significant amount of non-interest-bearing deposits sitting on banks› balance sheets.”

Supporting the ratings, S&P further said banks in the GCC continue to display strong capitalization by global standards, albeit with signs of qualitative deterioration. Over the past year, “we have affirmed ratings on most of the 24 banks we rate in the GCC. We have taken a few negative rating actions, most of them on banks in Bahrain and Qatar. We upgraded one bank in the UAE based on our view of its higher systemic importance and higher expected government support. Overall, 25% of our rated banks in the GCC currently have a negative outlook, two-thirds of which are in Qatar, due to the potential effect of the boycott on Qatari banks› funding profiles, asset quality, and profitability.

There are also a couple of other banks elsewhere in the GCC, where higher risks from their international operations drive our negative outlook.”

Moreover, higher oil prices and stronger public investments are resulting in higher economic growth across the GCC in 2018. “We forecast that oil prices will stabilize at about $65 per barrel in 2019 and $60 I 2020, and we anticipate unweighted average economic growth of 2.8% in 2019-2020 for the six GCC countries. This is less than a half of what they delivered in 2012, but more than five times higher than their performance in 2017.

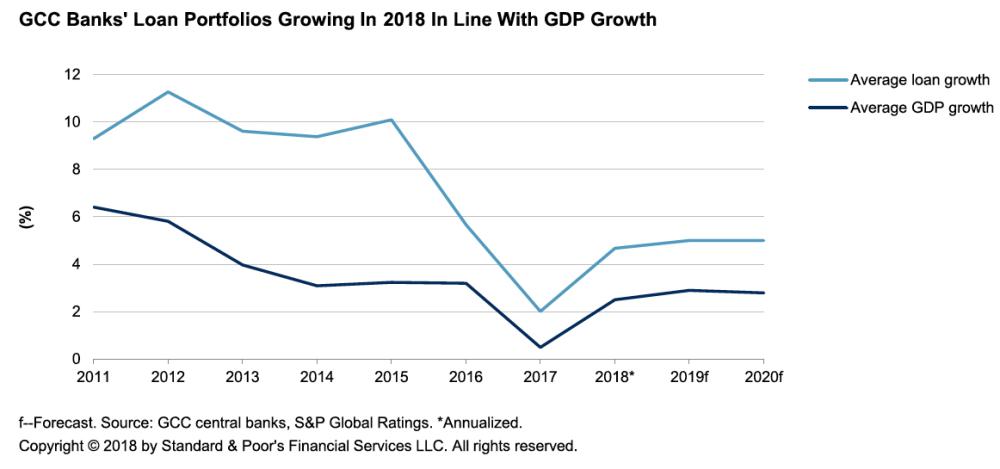

Growth in lending recovered slightly, reaching an annualized 4.7% at midyear 2018. We expect a slight acceleration in the next two years barring any unexpected shock. “Higher government spending, supported by strategic government initiatives, will support the lending growth.

Nevertheless, a surge in geopolitical risk or a significant drop in oil prices, and ensuing delays of some of these initiatives and in overall consumer confidence, could severely affect our base-case scenario,” the report noted.

As of June 30, 2018, NPLs to total loans for the rated GCC banks reached 2.6%, compared with 2.4% at year-end 2015. A combination of write-offs and restructuring of exposures to adapt to the new economic reality explain this stable stock of problematic assets. Restructured loans and past due but not impaired loans saw a higher increase, reflecting corporate entities› longer cash flow cycles and challenges related to specific economic sectors, such as the real estate and hospitality sectors.

With the transition to IFRS 9, the amount of problematic loans (Stage 2 and Stage 3 loans) stood on average at around 16% of total loans for banks that reported these numbers. However, a few top tier banks and a couple of banks that benefit from a niche position displayed stronger metrics.

Top-tier Saudi and Emirati banks fared relatively better. NPL coverage ratios increased mechanically, due to the adoption of IFRS 9, reaching 179% at June 30, 2018. Given the intrinsic vulnerabilities of the GCC region, “we expect banks to continue increasing their provisioning levels.”

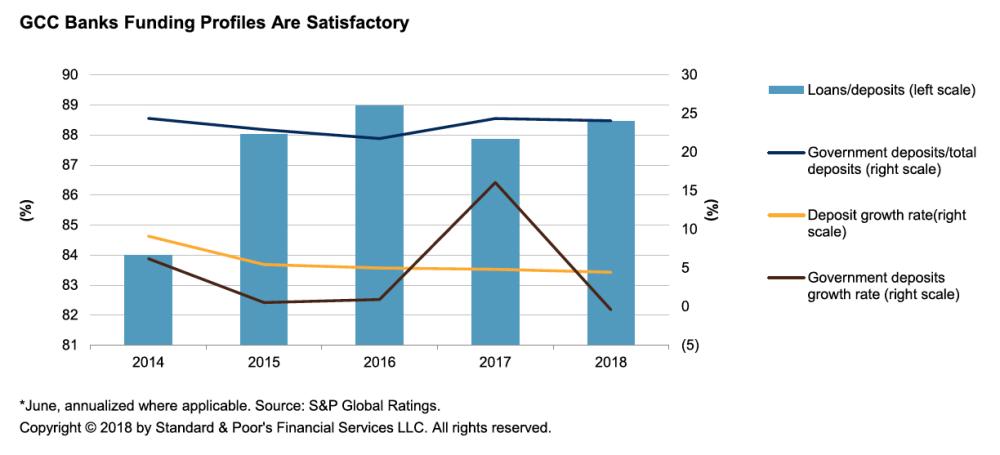

Furthermore, GCC banks› funding profiles are seen as satisfactory. Funding is dominated by core customer deposits, and the use of wholesale funding remains limited except for a few large and sophisticated issuers. The GCC banking system›s loan-to-deposit ratio averaged 88.4% as of June 30, 2018, compared with 87.8% at year-end 2017.

The ratio of cash and money market instruments to total assets remained stable over the past 18 months due to muted loan growth, still growing deposits, and the deployment of excess liquidity in government debt issuances. “We think that government issuances will continue to attract the attention of local and regional banking systems. As of June 30, 2018, the coverage of short-term wholesale funding by broad liquid assets stood at about 4.7x on average for rated GCC banks, compared with 3.7x at year-end 2016.” — SG