JEDDAH — The credit outlook for Gulf Cooperation Council (GCC) corporates is broadly stable, underpinned by a calm macroeconomic outlook, stable sovereign ratings, supportive interest rates, rising oil prices, and support from owners, S&P Global Ratings report on Monday said.

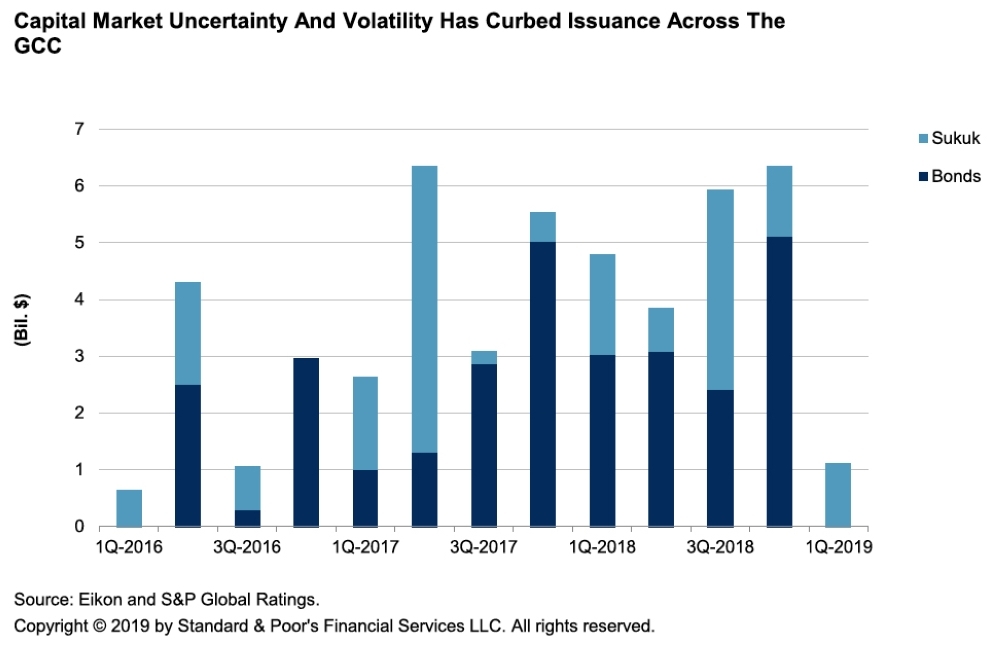

It said issuance volumes are likely to pick up strongly in the remainder of the year, led by Saudi Aramco and Saudi Telecom, though the GCC corporate and infrastructure capital market activity was slow in the first quarter of 2019, due to volatility in the global capital market.

Political risk, energy and water subsidies, and tax reforms across the GCC are the other key risks for the region›s issuers, the report added.

Nevertheless, S&P Global Ratings expects volumes to pick up strongly in the remainder of the year.

“We have seen visibly lower issuance by GCC corporates in the first months of the year. Total bond and sukuk issuance in the year-to-date is around $1.1 billion, and largely from two issuers--the Saudi food and beverage group Almarai Company, which came to the market with its debut $500 million five-year 5.95% sukuk, and a $600 million sukuk issued by Bahrain sovereign wealth fund Mumtalakat. This situation is likely to change in the coming days and months, with the likes of

Saudi Aramco and Saudi Telecom lining up to tap the international capital markets,” the report said.

Despite strong interest in credit ratings from previously unrated GCC-based corporates in new industries such as consumer goods, health care, and education, uncertainty and volatility in the global capital market have kept issuance volumes low so far in 2019, it said.

The report further revealed that the regional real estate markets remain under pressure, notably in Dubai and Qatar because of oversupply and waning demand.

Operating costs for many businesses have also been hit by increasingly demanding rules for the nationalization of the workforce, the report noted.

With average yields on GCC bonds and sukuk having falling in recent weeks to levels not seen since 2017, issuers see an opportunity to lock in lower rates on long-term borrowings.

The regional real estate markets, notably in Dubai, Qatar, and Saudi Arabia, remain under pressure due to a combination of continued oversupply and waning demand.

“We expect Dubai residential real estate prices to fall further in 2019, approaching levels last seen at the nadir of the 2009-2010 property crash, before a gradual stabilization in 2020, though without a meaningful recovery in 2021,” adding that “we continue to see political risk, energy and water subsidies, and tax reforms across the GCC as some of key near-term risks to the region›s issuer credit ratings.” — SG