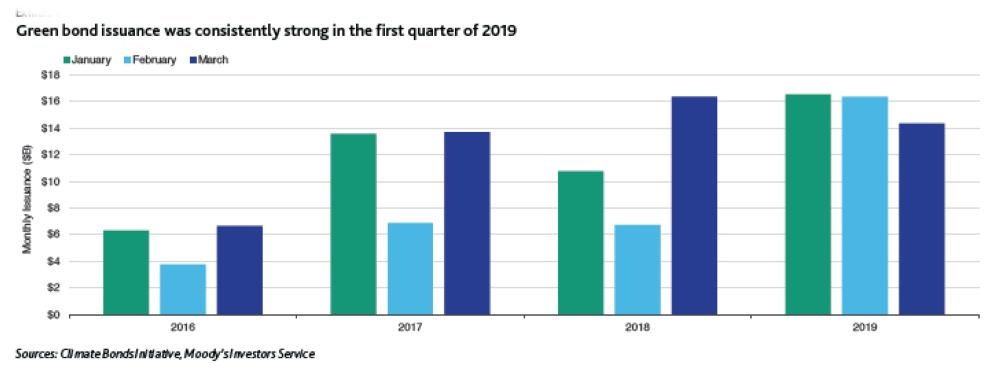

JEDDAH — Corporate issuers brought $47.2 billion of green bonds to market globally in the first quarter of 2019, a 40% increase over the first quarter of 2018, Moody’s Investors Service said in its “Sector In-depth” report released Wednesday.

This issuance level is a record for first-quarter green bond issuance, and trails only the fourth quarters of 2017 and 2018 for the largest quarterly issuance to date. Corporates, both financial and non-financial, as well as European issuers, were strong contributors to overall issuance. First-quarter issuance puts the market roughly in line to hit our 2019 forecast of $200 billion of total green bond issuance.

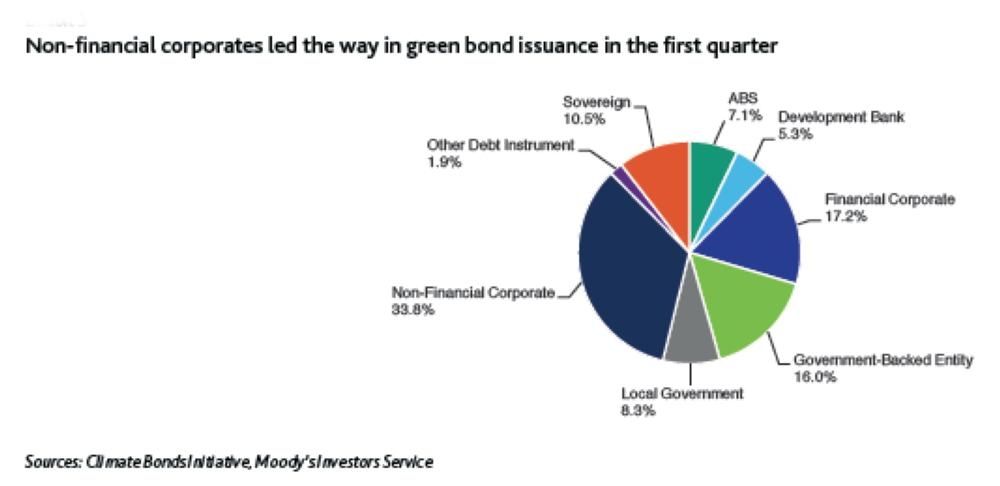

Q1 2019 green bond volume sets first-quarter record, with strong corporate issuance. Corporates were strong contributors to overall issuance, with $15.9 billion of non-financial corporate issuance and $8.1 billion of financial corporate issuance accounting for 34% and 17% of total volume, respectively.

According to the Global Sustainable Investment Alliance’s recently released 2018 Global Sustainable Investment Review, assets under management using sustainable, responsible and impact (SRI) investing strategies stood at $30.7 trillion globally at the start of 2018, a 68% increase from four years earlier.

Green sukuk and sustainable investing principles overlap, driving good long-term potential despite a slow start. We expect the Islamic finance sector's strong growth over the past 10 years to continue, reflecting that it remains underrepresented in the global financial system while demand for Shariah-compliant financial instruments is rising. This growth should translate into stronger prospects for green sukuk issuance, primarily by sovereigns and financial institutions.

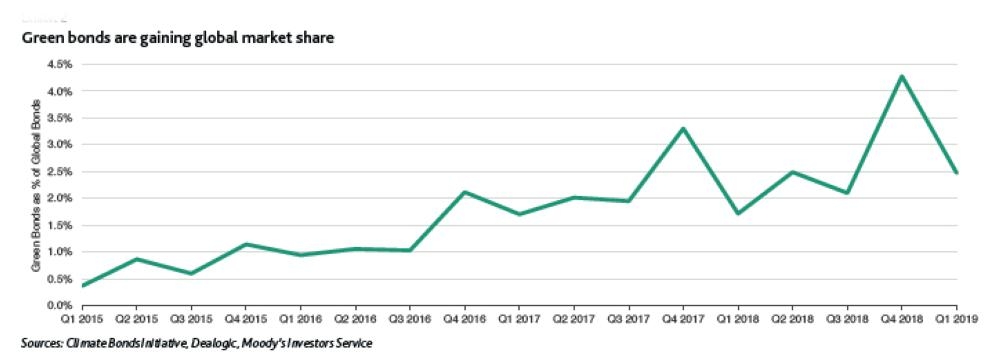

Issuers brought $47.2 billion of green bonds to market globally in the first quarter of 2019, a 40% increase compared with the first quarter of 2018. The issuance level is a record for first-quarter green bond issuance, and trails only the fourth quarters of 2017 and 2018 for the largest quarterly issuance to date. Corporates, both financial and non-financial, as well as European issuers, were strong contributors to overall issuance. First-quarter issuance puts the market roughly in line to hit our 2019 forecast of $200 billion of total green bond issuance.This strong issuance compared to Q1 2018 occurred despite a 3.2% decline in overall global issuance, according to Dealogic, continuing a trend under which green bonds have increased their share as a percentage of total bond issuance. Green bonds accounted for 2.5% of total first-quarter global bond issuance, up from 1.7% in the first quarters of both 2017 and 2018. We expect this trend to persist in the long run as the market continues to mature.

Corporates were strong contributors to overall issuance in the first quarter, with $15.9 billion of non-financial corporate issuance and $8.1 billion of financial corporate issuance accounting for 34% and 17% of total volume, respectively. Non-financial

corporate issuance was particularly strong and compared with 18% for the whole year of 2018. Local government and government backed entities accounted for a combined 24% of issuance, up from 15% for the whole of 2018.

Notable sectors in which issuance declined include development banks, which accounted for just 5% of issuance during the quarter, and asset-backed securities (ABS), which accounted for 7% compared with 15% for the whole of 2018. The latter primarily reflects relatively slow $2.5 billion issuance by Federal National Mortgage Association (Fannie Mae, Aaa stable), which has averaged almost $6 billion of quarterly issuance over the past two years.

Seven non-financial corporate issuers brought green bond tranches of $1 billion or more to market in the first quarter. The largest of these was MidAmerican Energy Company (A1 stable), which issued a $1.5 billion green bond in January. The first quarter also saw two notable telecoms green bonds, including a €1 billion green bond from Telefonica S.A. (Baa3 stable) and a $1 billion green bond fro Verizon Communications Inc. (Baa1 positive), issued just a few days apart in February.

European issuers accounted for approximately half of total green bonds in the first quarter, supported by over $8 billion of volume from French issuers alone (see Exhibit 4). French issuance was strongly supported by the largest issuer during the quarter, Societe du Grand Paris (Aa2 positive), which brought €2.1 billion of green bonds to market across three tranches, including a €2 billion tranche issued in March. A €1.7 billion green bond issued by the Government of France (Aa2 positive) in February also supported strong European and French issuance. France was one of three sovereigns to issue green bonds during the quarter: the Government of Poland (A2 stable) issued a €2 billion green bond in March and the Government of Indonesia (Baa2 stable) issued a $750 million green bond in February. North American issuers were also significant contributors to issuance in the first quarter, accounting for 31%, or $14.5 billion, up from 23% for the whole of 2018. This volume was largely driven by $11.2 billion of US-based issuance, supported by the issuances by Fannie Mae, MidAmerican Energy and Verizon. Other significant issuance by US-based issuers included a €1 billion green bond issued by Citigroup Inc. (A3 stable) in January.

Green bonds from Asia-Pacific issuers represented just 15% of total first-quarter issuance, down from 29% for the whole of 2018. This largely reflects a decline in issuance by Chinese issuers, with the $2.2 billion of total China-based issuance significantly trailing the average quarterly issuance of $7.8 billion for 2018. Beyond China, other Asia-Pacific issuers accounted for almost $5 billion of combined volume, with the largest deals coming from the Republic of Indonesia, noted above, and the Queensland Treasury Corporation (Aa1 stable), which issued an AUD1.25 billion green bond in March.

With Europe dominating issuance, euro-denominated green bonds accounted for 48% of the total volume, followed by US dollar-denominated issuance at 24%. Notably, Swedish krona-denominated issuance accounted for 11% of the total volume, supported by 36 individual transactions totaling more than $5 billion. In terms of use of proceeds, energy and buildings continued to lead in the first quarter, accounting for 28% and 26% of issuance, respectively. Notably, however, transport green bonds accounted for 24% of issuance, a significant increase compared with previous quarters. Diversification of use of proceeds is likely to continue as a growing variety of issuers participate in the green bond market.

Beyond green bonds, social and sustainability bonds continue to gain in prominence and grow at an accelerated rate.

Combined social and sustainability bond issuance totaled $13.4 billion in the first quarter, eclipsing the previous quarterly record of $10.2 billion in the third quarter of 2018. If the social and sustainability bond markets continue at the first quarter’s pace and eclipse $53 billion of combined issuance for 2019, this would represent a 74% increase over annual 2018 issuance. By way of comparison, the green bond market grew by just 7% annually last year.

The continued development of the larger sustainable investment universe will support green bond market growth in the long run. Investor demand for green and sustainable investing products continues to grow, and has to date outpaced the supply of such products. According to the Global Sustainable Investment Alliance’s recently released 2018 Global Sustainable Investment Review, assets under management using sustainable, responsible and impact (SRI) investing strategies stood at $30.7 trillion globally at the start of 2018, a 68% increase compared with four years earlier.

Japan has been the fastest growing region, while in Europe, where nearly half of global sustainable assets are managed, the market is showing signs of maturation. Although total SRI assets under management in Europe have continued to grow, their share of the overall professionally managed assets in the region fell to 49% in 2018 from 59% in 2014, a trend the Global Sustainable Investment Alliance suggests may reflect stricter standards in the region. SRI assets have continued to gain market share in North America, however, rising to 51% from 31% in Canada between 2014 and 2018, and to 26% from 18% in the United States.As investors increasingly look to incorporate Environmental, Social and Governance (ESG) factors into their investment strategies, more businesses are voluntarily disclosing key information in these areas. For example, the United Nations Global Compact, which publishes a set of principles for corporate sustainability, saw the number of participating companies that voluntarily report on their work to embed these principles in their operations increase to 5,017 in 2013 from 167 in 2004. Meanwhile, many issuers are now linking their business objectives to the United Nations Sustainable Development Goals (SDGs), a trend we expect will continue as companies increasingly align their business models with sustainable development scenarios. Correspondingly, sustainability reporting practices will continue to evolve in terms of extent and quality.

As demand for responsible investing strategies grows and as more issuers focus on sustainability, new and innovative financial products will continue to enter the marketplace. For example, the labeled bond market in recent years has expanded to include social and sustainability bonds which allow issuers to finance projects beyond those with green or climate objectives. There has also been growth in ESG-linked loans, which tie the interest rate on a loan to the borrowing company’s performance on specified ESG metrics. In early 2018, for example, Dutch bank ING Bank N.V. (Aa3 stable, baa14) issued such a loan to Wilmar International, a Singaporean palm oil producer.

In March 2019, the Loan Market Association, the Asia Pacific Loan Market Association and the Loan Syndications and Trading Association published the Sustainability Linked Loan Principles, voluntary recommended guidelines to be applied to loan instruments and/or contingent facilities seeking to incentivize the borrower’s achievement of defined sustainability performance targets. "We expect ESG-linked loans to grow in popularity following the publication of these guidelines, in the same way that the development of applicable standards by the International Capital Market Association has supported green, social and sustainability bond markets." — SG