JEDDAH — Turkey's Islamic banking assets are set to double within 10 years from a low level as government initiatives drive growth in the sector, Moody's Investors Service said in a report published Monday.

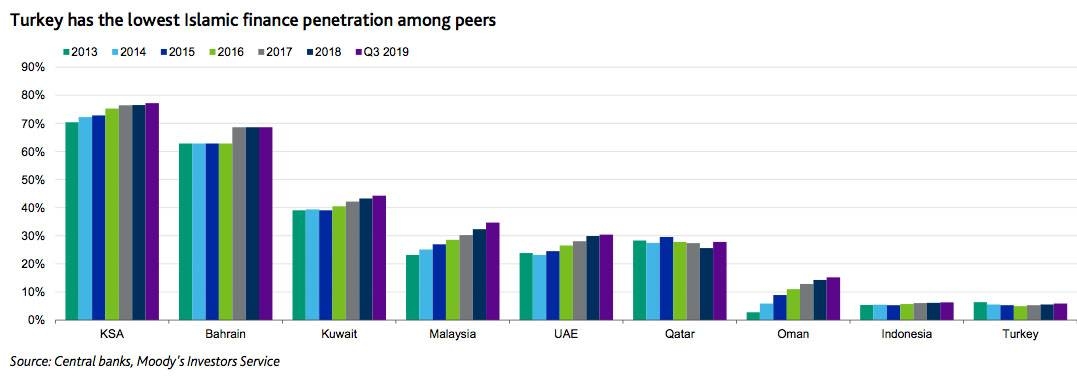

Turkey's Islamic finance sector currently is smaller than other large Muslim countries, and its slow start means it has ample room to expand. The sector represented just over 5.8% of banking assets at the end of September 2019, compared to Malaysia (33%) and Middle Eastern countries (15% - 77%).

More than 95% of Turkey's roughly 83 million population is Muslim but Islamic finance penetration in the country is very low. The aggregate market share of Turkey's participation banks was 5.8% in September 2019, compared with an average penetration rate of 43% in other Middle Eastern countries and Malaysia.

The main reason is the relatively small number of Islamic banks and their limited distribution networks within Turkey. The sector market share has stagnated around 5.5% since 2014,1 lagging the 6 percentage points average increase in the penetration rate recorded in other Muslim countries.

Islamic banks are called participation banks in Turkey and are regulated by the Banking Regulation and Supervision Agency (BRSA). They are required by law to become a member of the Participation Banks Association of Turkey (PBAT) - an umbrella organization defending the rights and interests of the country's Islamic banks. PBAT targets an Islamic banking penetration of 15% by 2025.

Islamic deposits (under Shariah law these are defined as investment accounts or funds collected) benefit from the same protection as conventional bank deposits under Turkey's deposit insurance and protection scheme. This enables them to attract funds from non- Muslim depositors.

There are six Islamic banks in Turkey. Three - Kuveyt Turk Katilim Bankasi A.S., Turkiye Finans Katilim Bankasi A.S. and Albaraka Turk Katilim Bankasi A.S. - have large shareholdings by Middle Eastern lenders. They dominate the sector with a combined market share of 76% of Turkey's Islamic banking assets at the end of June 2019.

During the two years period between 2014 and 2015, the Turkish government established two new state-owned participation banks and their market share is increasing. The new state-owned domestic lenders have intensified competition in the industry and are broadening the base of Islamic banking service provision. They are gradually building out extensive branch networks that will attract increasing numbers of Islamic banking customers in the coming years.

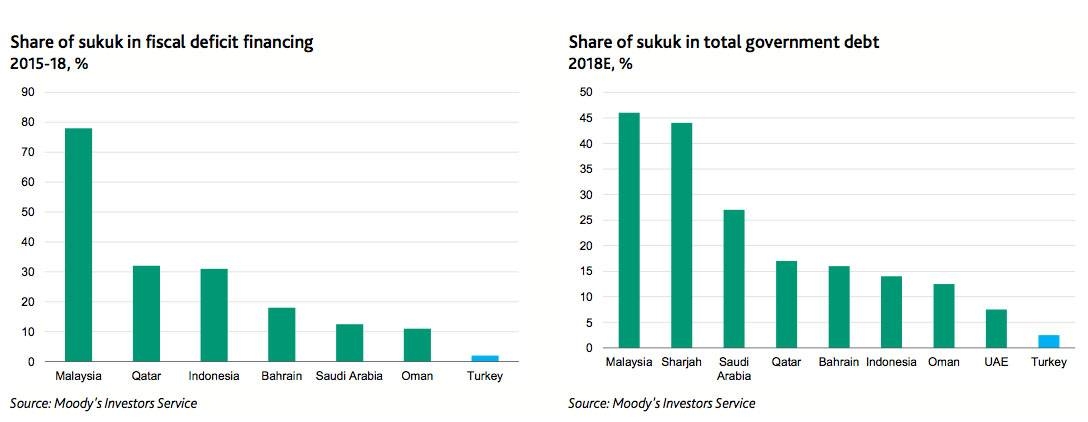

The Kuwaiti-owned Kuveyt Turk issued the first sukuk in Turkey in 2010 with a face value of $100 million. Total sukuk issuance by Turkish Islamic banks amounted to TRY45 billion by the end of 2018. Annual sukuk issuance volume in 2018 was more than TRY16 billion ($2.7 billion), many multiples of the amount recorded at the start of the decade.

The Turkish government made its debut sukuk issuance in 2012, with two issues, one domestic and one in foreign capital markets. Since then the Treasury has issued around TRY30 billion in the domestic market and $6 billion in international markets as a means to diversify its funding sources and attract capital from the Gulf Cooperation Council and other countries.

The level of Islamic banking assets in Turkey remains low, however, there is ample room for the sector to grow. With the sector's strategic importance for the Turkish government, dynamics of Islamic finance and banking are evolving and foundations for a period of significant Islamic finance growth are being laid. We expect Islamic banking to play a key role in Turkey's development of financial services over the next decade.

Turkey's ambition is to establish Istanbul, the country's largest city and its economic powerhouse, as a global financial center. It aims to raise the share of financial services in Turkish GDP to 6% by 2023 from 3% at the end of 2018. Development of Islamic banking and finance is one of the key pillars set out in the seven-pillar framework called the Istanbul International Financial Centre Strategic Action Plan.

Policies listed under the plan's Islamic finance pillar include raising public awareness of Islamic finance and banking, establishing training to produce staff qualified in Islamic financial law and practices and broadening the range of Islamic financial products and services on offer to the Turkish population. The government has mandated Participation Banks Association of Turkey and the Banking Regulation and Supervision Agency (BRSA) to oversee or contribute to most of the Islamic finance policies listed in the IIFC strategic plan.

The PBAT is targeting a penetration rate of Islamic banking of 15% by 2025 and has put forward its own Strategic Action Plan outlining how it aims to achieve its targets.

The government established two state-owned Islamic banks, Ziraat Katilim and Vakif Katilim in 2014 and 2015, respectively. While Vakif Katilim has a separate brand than the state-owned Vakifbank (B2 negative, caa2), Ziraat Katilim shares the same branding as state-owned conventional bank T.C. Ziraat Bankasi A.S. (Ziraat) (B2 negative, caa1), the largest bank in Turkey as of June 2019. Nevertheless, the association with their shareholder is a positive factor that will support its future growth ambitions.

In 2019, the government established a third Islamic bank, Turkiye Emlak Katilim Bankasi, bringing the number of banks operating under the principles of Shari'ah law to six. The market share of the state-owned domestic banks in Turkey increased by three percentage points in the first half of 2019, standing at 24% of total Islamic banking assets in June 2019.

Increasing competition as well as the presence of state-owned banks with vast distribution networks in the industry is contributing to the growth of Islamic finance and banking and broadening the range of Islamic products and services. — SG