By Ole Hansen

The below summary highlights futures positions and changes made by hedge funds across 24 major commodity futures up until last Tuesday, March 24. During this period the dash-for-cash phenomenon slowed and individual commodities began reaction to the shocks currently hitting both supply and demand.

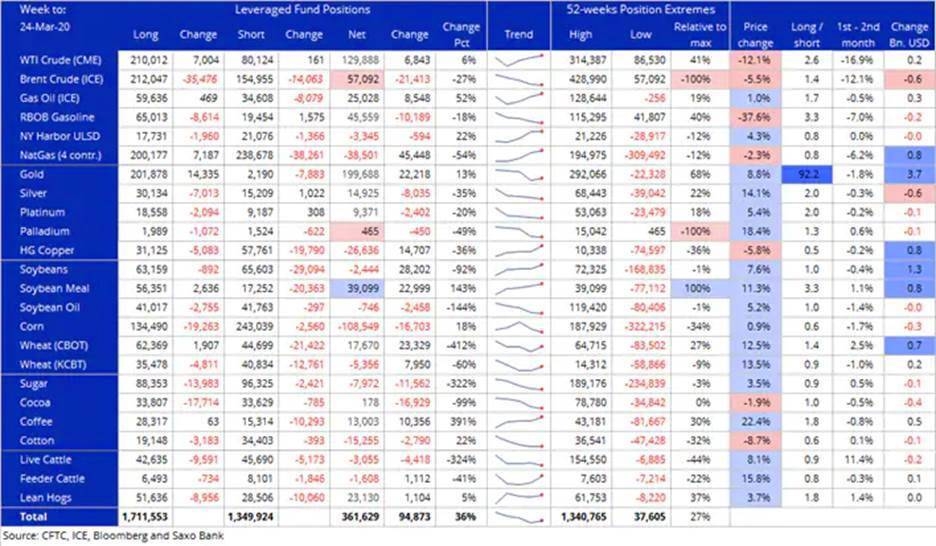

Funds increased bullish bets for the first time in five weeks by 36% to 361k lots. In demand were natural gas, soybeans, wheat and coffee while selling hit Brent, silver, corn, sugar and cocoa.

Despite suffering another week of steep price losses, the energy sector only saw modest changes. WTI crude oil was bought for a third week to the tune of 7k lots while selling of Brent crude oil extended to a fourth week.

The selling of 21k lots took the net-long to just 57k lots, the lowest since November 2014. Overall the combined net-long reached 187k lots, a near 8 year low. While the WTI crude oil position has risen by 7k lots during the past four weeks, Brent has seen its net-long tank by 231k lots.

This divergence is, however, likely to correct as the US become the epicenter of the corona virus outbreak. With that demand will suffer and stocks rise. Up until now Brent crude oil, the global benchmark, has been the contract used to reflect the negative price impact of a Saudi price war, slump in demand and spike in stocks.

Natural gas saw continued buying with the net-short having been cut by 88% during the past six weeks. All of this happening while the price continues to linger near the lowest level in almost 25 years.

The dramatic squeeze in the gold basis between the OTC spot priced in London and the COMEX futures in New York was captured in the data last week. Despite rallying by close to 9% the net-long only rose by 13% to 200k lots. Most pronounced was the collapse in the gross short positions to just 2,190 lots, a ten-year low.

Silver’s net-long was cut by 35% in a delayed reaction to the near 30% price slump in the previous reporting week. Bearish HG copper bets was cut by 36% as short covering started to emerge after the price found support at $2/lb.

CBOT Wheat and Arabica coffee, two of the best performing commodities, both saw strong buying as the prices jumped 12.5% and 22.4%. Both however were primarily driven by short-covering and it highlights a current unwillingness to add exposure. Cotton, a major looser as clothes stores remain closed around the world, was sold while the unwinding of long cocoa bets finished after the net position hit neural and the price looked for support at $2200/t.

The soymeal net-long jumped 143% as a Chinese soy meal shortage for its livestock industry supported a short-term bullish outlook. Sugar and corn both sold in response to lower demand from ethanol producers as crude oil slumps and fuel stocks rise.

What is the Commitments of Traders report?

The Commitments of Traders (COT) report is issued by the US Commodity Futures Trading Commission (CFTC) every Friday at 15:30 EST with data from the week ending the previous Tuesday. The report breaks down the open interest across major futures markets from bonds, stock index, currencies and commodities. The ICE Futures Europe Exchange issues a similar report, also on Fridays, covering Brent crude oil and gas oil.

In commodities, the open interest is broken into the following categories: Producer/Merchant/Processor/User; Swap Dealers; Managed Money and other.

In financials the categories are Dealer/Intermediary; Asset Manager/Institutional; Managed Money and other.

Our focus is primarily on the behavior of Managed Money traders such as commodity trading advisors (CTA), commodity pool operators (CPO), and unregistered funds.

They are likely to have tight stops and no underlying exposure that is being hedged. This makes them most reactive to changes in fundamental or technical price developments. It provides views about major trends but also helps to decipher when a reversal is looming.

— the writer is head of commodity strategy at Saxo Bank