The COVID-19 pandemic and the collapse of oil prices will test the earnings of rated banks in Gulf Cooperation Council (GCC) countries. S&P Global Ratings believes that rated banks' profitability and provision cushions built over past years will help them navigate the current rough waters.

Most rated GCC banks have relatively strong profitability and a conservative approach to calculating and setting aside loan-loss provisions. Some banks, for example those in Kuwait, take a conservative approach as part of local regulatory requirements to set aside general provisions for all their lending portfolios.

Overall, we estimate that rated GCC banks could absorb up to a $36 billion shock before starting to deplete their capital base. This corresponds to about 3x our calculated normalized losses, which implies a substantial level of stress in our view.

We base our study on a sample of 23 rated commercial banks in the GCC with exposures predominantly concentrated in GCC countries. At year-end 2019, these banks' total assets reached $1.5 trillion.

In our study, we focus on rated GCC banks' lending portfolios when it comes to estimating the additional provisions. Given that the GCC banks we rate take a relatively conservative approach toward the quality of their investment portfolios, we think that some of them stand to benefit from capital gains due to the shift in market conditions.

S&P Global Ratings acknowledges a high degree of uncertainty about the rate of spread and peak of the coronavirus outbreak. Some government authorities estimate the pandemic will peak about midyear, and we are using this assumption in assessing the economic and credit implications.

We believe the measures adopted to contain COVID-19 have pushed the global economy into recession. As the situation evolves, we will update our assumptions and estimates accordingly.

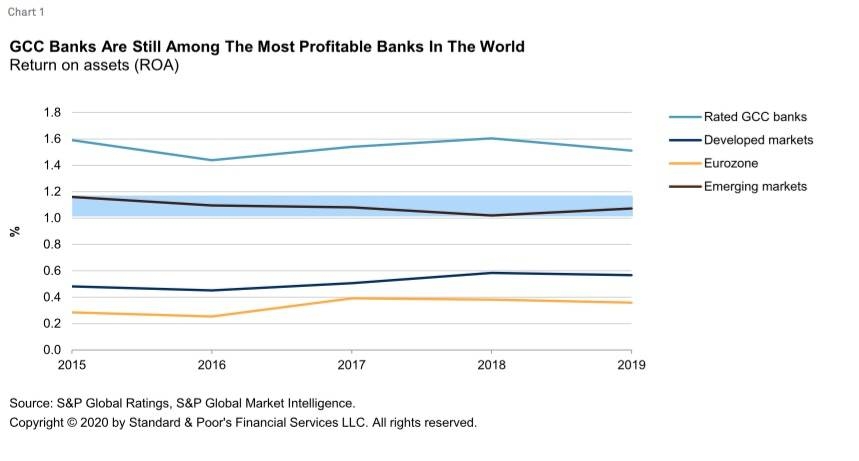

Rated GCC Banks Are Highly Profitable

Although we have observed a slight decline over the past couple of years, rated GCC banks' profitability still compares favorably in an international context (see chart 1).

Chart 1

Three factors explain this strong structural profitability:

• A large portion of noninterest-bearing deposits, which explains why banks' margins are hefty. At year-end 2019, rated GCC banks' net interest margin stood at 2.9%. Moreover, rated GCC banks' revenue remain skewed toward interest income, which represented three quarters of total revenue at year-end 2019 (see chart 2).

• Noninterest revenue mainly comes from sustainable sources of income such as fees and commissions (a lot of which is related to loan inception or foreign currency exchange), with limited contribution of volatile market-related income.

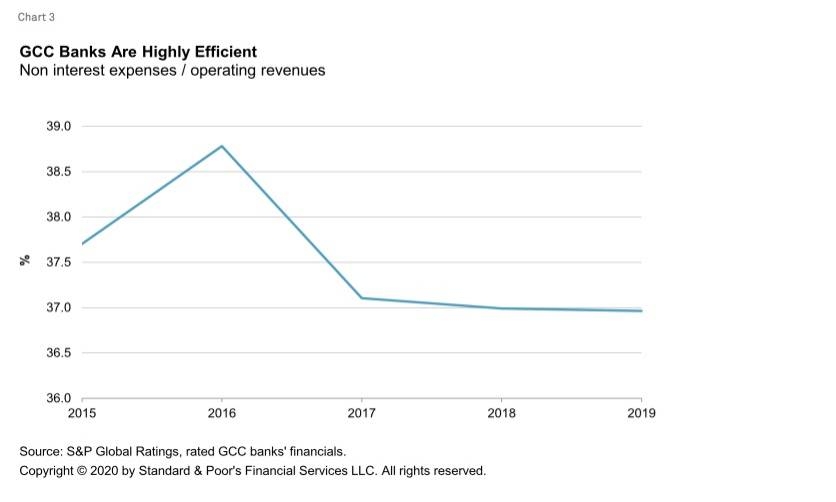

• Banks' efficiency is very strong. The average cost-to-income ratio for rated GCC banks reached 37% at year-end 2019. This low level is explained by low cost of labor, the absence of taxes and social contributions (except for nationals of the GCC countries), and a stringent approach toward cost control through small branch networks and leveraging technology for customer service.

How resistant are Gulf banks to the COVID-19 pandemic?

We anticipate banks' profitability will deteriorate in 2020, because of the dual shock of COVID-19 and the decline in oil prices. This is because financing growth will remain limited, with banks focusing more on preserving their asset-quality indicators than generating new business.

We also believe the interest margin will decline, given the reduction in interest rates and the structure of rated GCC banks' funding profiles (with a significant contribution of noninterest-bearing deposits). Furthermore, we expect asset quality will deteriorate and cost of risk will increase.

In our view, the support measures enacted by GCC governments will at best delay this problem, in the absence of additional measures. However, we believe banks will continue to benefit from their relatively low cost base and potential additional cost-saving initiatives from 2021.

Some banks announced employment-preservation measures for 2020 but cuts will probably come next year if the environment doesn't improve. Investment revenue is also likely to support the bottom line of some banks this year as the drop in interest rates increases the market value of these instruments and banks decide to offload them, thereby realizing gains.

Our current assumption is that of COVID-19 containment and the resumption of nonoil activity will occur by third-quarter 2020. Should this take longer, it would mean lower profitability and even losses for some banks.

How much can rated banks take?

As part of its risk-adjusted capital framework, S&P Global Ratings calculates "normalized losses." Based on our observations of credit losses during past economic downturns, we believe that credit losses could take up to three years to flow through a bank's financial statements, except for credit cards.

We estimate normalized losses based on the difference between our idealized losses (see "Related Criteria") and the unexpected losses that we use to calibrate our capital charges. Normalized losses are calculated based on an economic cycle of 12 years including three years of recession.

In our view, product pricing and provisioning should be able to absorb an average or "normal" level of annual credit losses, which we refer to as normalized losses, and banks hold capital to absorb losses that are greater than this "normal" level. In order to assess the cost related to COVID-19, we started with our normalized losses and tested the profitability of rated banks.

How do normalized losses compare with actual losses?

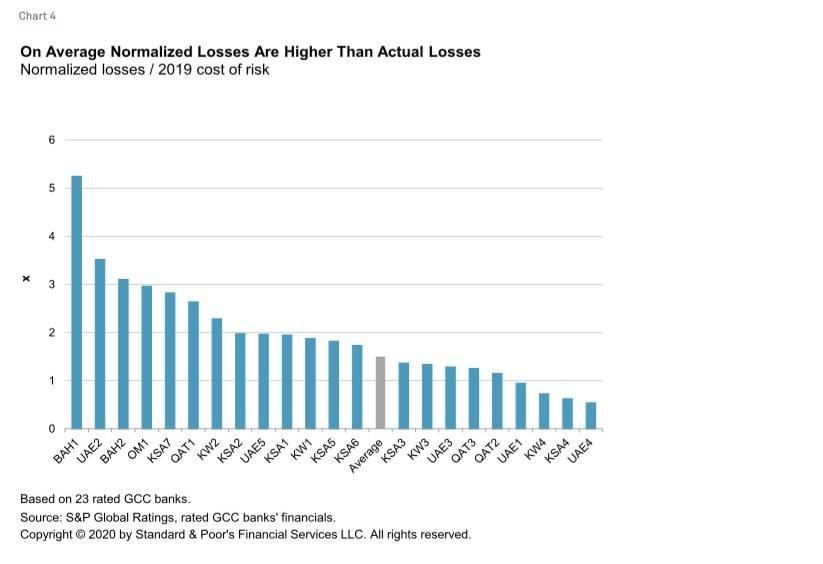

On average, our estimates of normalized losses reached 1.5x banks' reported cost of risk in 2019. This average masks significant differences between the banks. The highest amount was for a Bahraini bank, given our more negative view on economic risk for Bahrain and this bank's exposures to riskier countries.

The following five banks have some exposure to riskier countries than the GCC or sectors such as real estate or small and midsize enterprises. For a few banks, the estimated normalized losses were lower than the actual cost of risk, which is due to either legacy exposures and ongoing cleanup or banks' conservative approach toward provisioning (see chart 4).

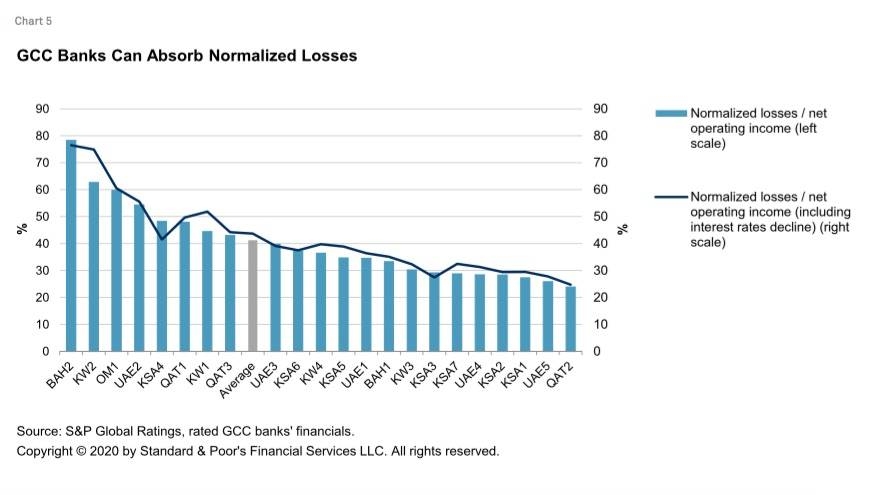

Rated banks have sufficient capacity to absorb normalized losses

At year-end 2019, all rated GCC banks had the capacity to cover normalized losses using their net operating income. This remains valid even if we factor in the impact of a 100 basis point (bps) drop in interest rates as reported by banks.

Over the past few weeks, we have observed significant moves from leading central banks to counterbalance the negative impacts of COVID-19 on the global economy. The US Federal Reserve reduced interest rates by 150 bps for example and this reduction was fully or partially mirrored by central banks in the GCC region as for most of them, there is a peg between their currencies and the US dollar.

We therefore decided to capture the potential impact of a 100-bps decline in interest rates. It is important to mention that within our sample, normalized losses represent more than 50% of net operating income for only five banks (seven banks if the decline in interest rates is included).

Chart 5

On average, GCC banks can absorb 2.7x normalized losses, but this masks a significant level of difference between banks. The most resilient are the Saudi banks and the least resilient are Bahraini banks.

Kuwaiti banks show lower resilience than banks in Qatar or the United Arab Emirates (UAE) because of their high exposure to the real estate sector (which attracts higher normalized losses under our methodology).

Qatari banks' normalized losses are also inflated by the exposure of some leading players to riskier markets such as Egypt and Turkey.

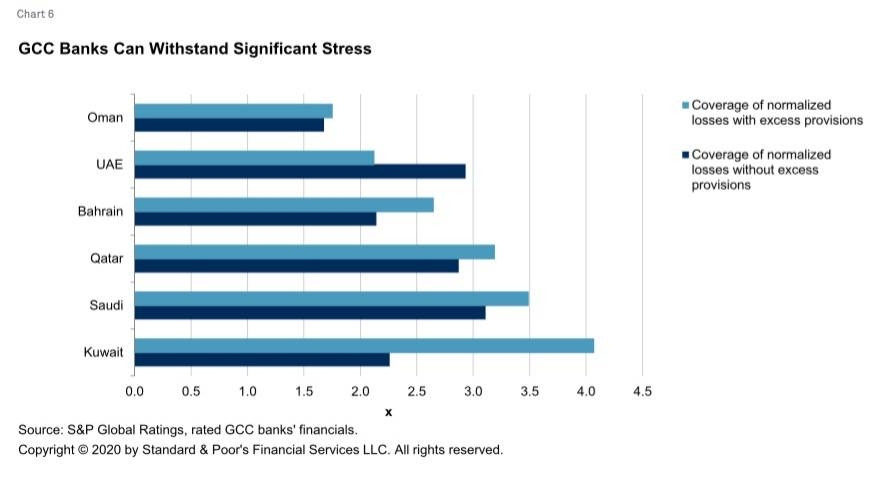

Looking at the coverage level using profitability gives only one side of the story. The other side can be uncovered by adding or subtracting the excess or shortfall in provisions. We define this as the total amount of provisions needed or held in excess of 100% coverage ratio.

Factoring in this cushion would show that Kuwait has the highest capacity to resist any increase in cost of risk and that Bahrain, Oman, and UAE are the most vulnerable in the current crisis.

This also explains why, under our base-case scenario, we expect the current crisis to remain a profitability shock rather than a capital event.

On average and factoring in the additional cushion, GCC rated banks can absorb 2.7x the normalized losses level without touching their capital base, which would correspond to a substantial level of stress in our view (see chart 6).

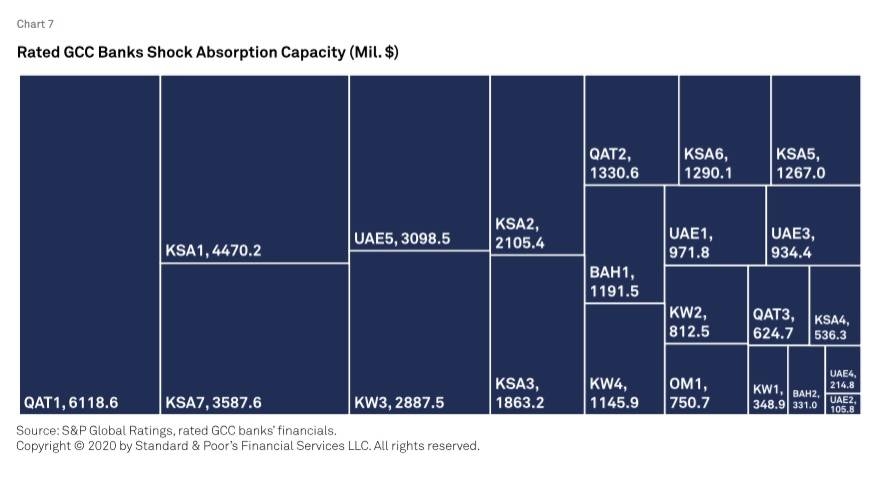

In absolute numbers, this corresponds to additional provisioning needs of $36 billion under the assumptions that nonperforming loans will be 100% covered by provisions and that the impact would be taken upfront and not amortized over several years.

However, it is also worth mentioning that this $36 billion is not uniformly distributed and that a few banks have bigger capacity to absorb losses than others do (chart 7). Moreover, this capacity is not correlated with the bank's size. — Standard & Poor’s Financial Services LLC