By Peter Garnry

DUBAI — In this equity note we highlight that US equities might soon be peaking against European equities on ground of relative total return performance, valuation differences and that European equities could benefit from an edge in green energy technologies and health care compared to the US. We also highlight the smaller technology sector weight as a potential catalyst for European equities over time.

US equities have shown an extraordinary rebound since March lows compared to European equities driven by strong price action in technology and biotechnology stocks. As we have said many times over the past weeks we guess that an enormous speculative retail flow in the US is behind most of the price action and thus pushing valuations to very high levels.

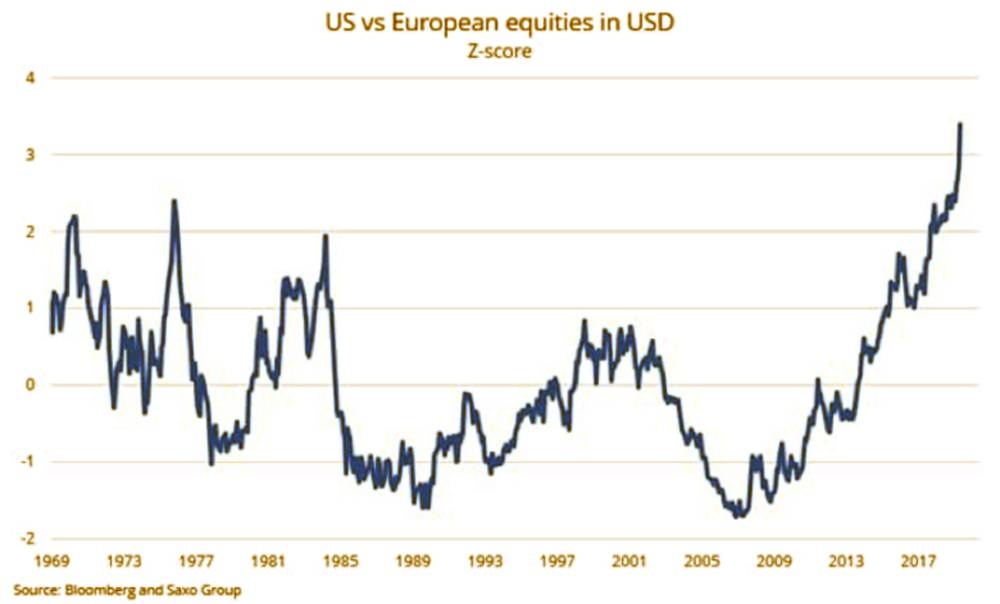

The disconnect between fundamentals and sentiment has pushed US equities to an extreme outperformance relative to Europe that one has to ponder whether this can continue.

The relative total return indices in USD between US and European equities have moved to 3.4 standard deviations indicating that US equities have drifted significantly away from its long-term relationship to European equities. The last extreme US outperformance has happened since September 2017 where US equities are up 20% and European equities are down 14% in USD terms.

European equities reached its peak outperformance against US equities around the end of 2007 but since then the fortunes have changed. US equities are up 140% and European equities are down 4% in USD terms. Two major events happened in the subsequent period.

The trade-weighted real USD rose 28% adding tailwind for US assets relative to non-US assets and the technology sector went through a massive boom through search engines (online advertising), smartphones, social media, video streaming, cloud-based application software, cloud-based infrastructure, machine learning and its related chip infrastructure, e-commerce platforms and online shopping.

The US had the upper hand in the recent technology boom with Silicon Valley financing technology ventures that managed to gain wide dominance before Europe’s fragmented technology hubs could come up with alternatives. Many of these emerging technologies had economics of scale that had not been seen since the 1960s industrial boom and the 1980s energy boom.

European equity markets were basically living in the past. A final important driver was that US companies were in general net buyers of their own shares where European companies continued to be net issuer of equity capital.

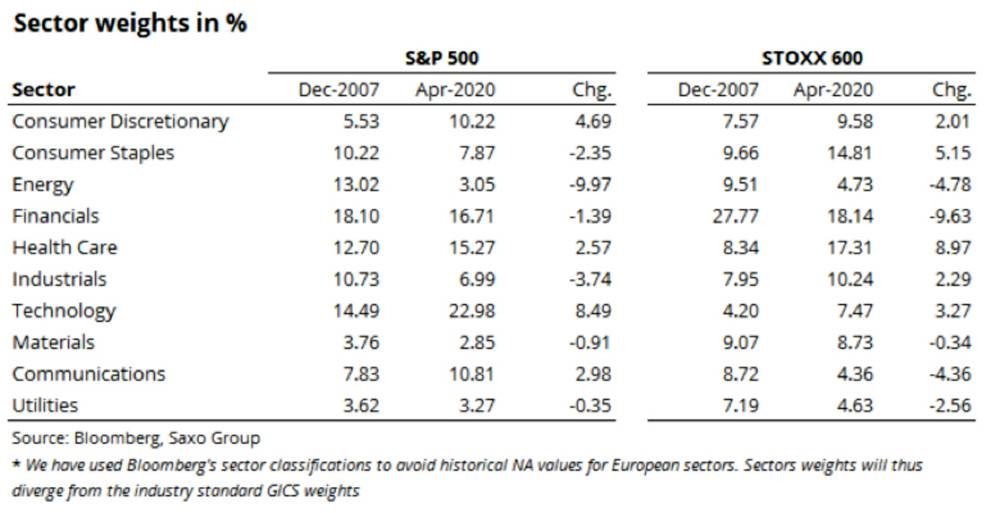

Changes in sector weights for S&P 500 and STOXX 600 since December 2007 is shown. While the collapse in the US energy sector has been significant it has been outweighed by the rise in technology (Microsoft and Apple), consumer discretionary (Amazon) and communications (Facebook and Alphabet).

The biggest losing sector in Europe has been the financials which were dominant in 2007, but is still the largest sector, but has since lost its profitability as the Euro crisis and wrong policies have made it difficult to operate banks. Europe’s two biggest winners have been health care stocks and consumer staples and here lies some of the future potential.

What is the case for being positive and overweight European equities? Valuation is much better on European equities with a forward dividend yield of 2.8% and dividend futures expecting annualized dividend growth of 0.6% until 2023.

On top of that the P/E multiple is lower on European equities relative to US equities so European equities could get a relative better P/E multiple over the coming years. US equities are currently priced with a forward dividend yield of 1.7% and dividend futures expecting negative 3.3% annualized dividend growth until 2023.

This means that US equities need P/E multiple expansion much more than European equities to continue to deliver outperformance. That’s going to be difficult.

In the case economic activity is subdued globally the coming years European equities offer more defensive characteristics with a higher weight on consumer staples, health care and utilities. Europe is leading on the green transformation and here lies another upside through the industrials and utilities sectors.

With only 7.5% of European equities in the technology sector there’s also room for a higher weight over time which will improve the growth profile of European equity markets. Finally with Europe’s large health care share and the increased focus on drug discovery and health care equipment after COVID-19 Europe does have an edge.

On the macro side a weaker USD, which is urgently needed by many countries, would add tailwind for non-US equities. Europe’s potential fiscal integration with the EU Commission issuing joint debt has the potential to solve some of Europe’s structural issues, which also could be a positive for European equities. Increasing technology regulation could also increase costs for US technology companies and thus act as a drag on US equities.

— The writer is head of equity strategy at Saxo Bank