DUBAI — As regulators and policymakers around the world seek to establish a more sustainable, stakeholder-focused, and socially responsible financial system for the future, S&P Global Ratings notes there are certain similarities between Islamic finance and sustainable finance.

Islamic finance abides by the goals and objectives of Shariah, and has some overlap with environmental, social, and governance (ESG) considerations and the broader aim of sustainable finance. Although this may sound obvious for environmental aspects through green sukuk and governance aspects through the presence of additional governance layers, the social aspect has until now been less obvious.

The spread of COVID-19 and countermeasures to slow its spread have significantly slowed the core Islamic finance economies. As a result, we expect unemployment rates to increase, with a consequent significant loss of income for households as companies implement measures to reduce their costs amid declining revenue.

The Islamic-finance industry has been talking about the potential to use the social instruments of Islamic finance to help address the impact of COVID-19 on corporates and banks through unremunerated or subsidized liquidity to help them cope with the short-term loss in revenue and allow them to preserve employment.

Social instruments could also be used directly to support households by compensating them for lost income, and by providing access to affordable basic services, such as education and health care.

From a credit rating perspective, in our opinion, banks' use of social instruments would have a limited effect on their balance sheets, as long as such instruments did not significantly reduce their profitability or increase their costs materially.

The social nature of sukuk would have no bearing on the instrument's creditworthiness as long as the social measures did not change the sponsor's obligation to pay sufficient amounts for the periodic distribution and principal reimbursement.

COVID-19 is causing a major slowdown in core Islamic finance markets and a spike in unemployment. Over the past three months, data show that the measures designed to curb the spread of COVID-19 are having a negative economic impact and worsening the business and financial positions of core Islamic finance countries.

• Service sectors will be hit harder than manufacturing sectors;

• Discretionary consumer spending will be hit harder than spending on necessities; and

• Smaller businesses will be hit harder than larger ones.

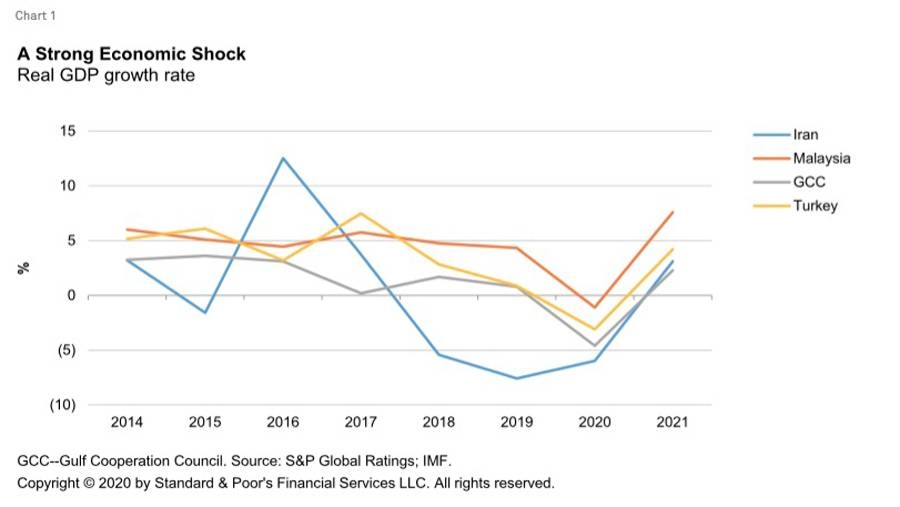

In particular, lockdowns and social distancing constraints are damaging countries' economies and we think that certain core Islamic finance countries will be hit hard in 2020 (see chart 1).

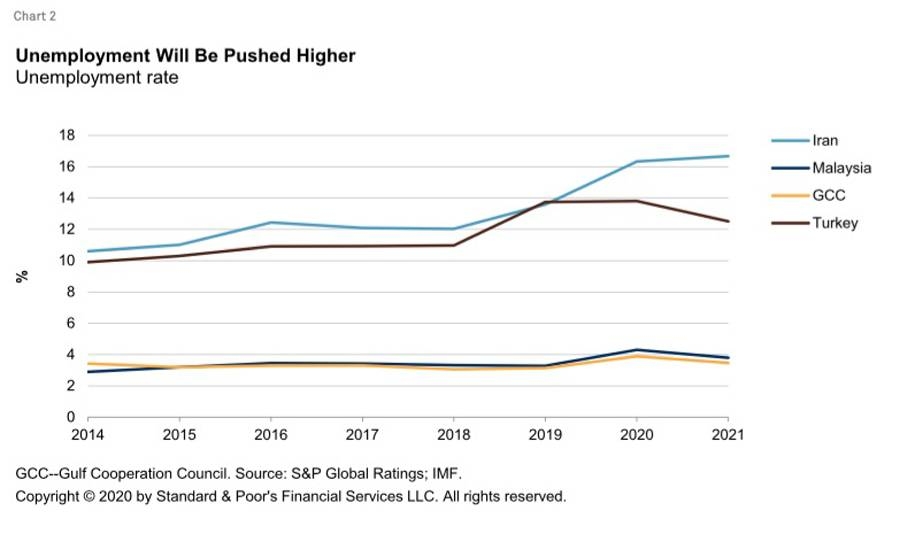

The economies of these countries are either dependent on commodities or on services. They are also less industrialized than countries in more developed markets and have smaller corporate sectors typically dominated by small and midsize enterprises (SMEs). We think it likely that unemployment rates and household loss of income will rise in some of these countries (see chart 2).

The fact that foreign workers represent the majority of the working population should somewhat offset the increase in unemployment in the Gulf Cooperation Council (GCC), because many foreigners will likely return to their home countries if they are furloughed or laid off.

In addition, government intervention through various support measures should somewhat counterbalance the negative effects of higher unemployment. For example, some GCC governments announced they would cover the private sector salaries of their nationals — and in some of the countries the salaries of foreign workers as well.

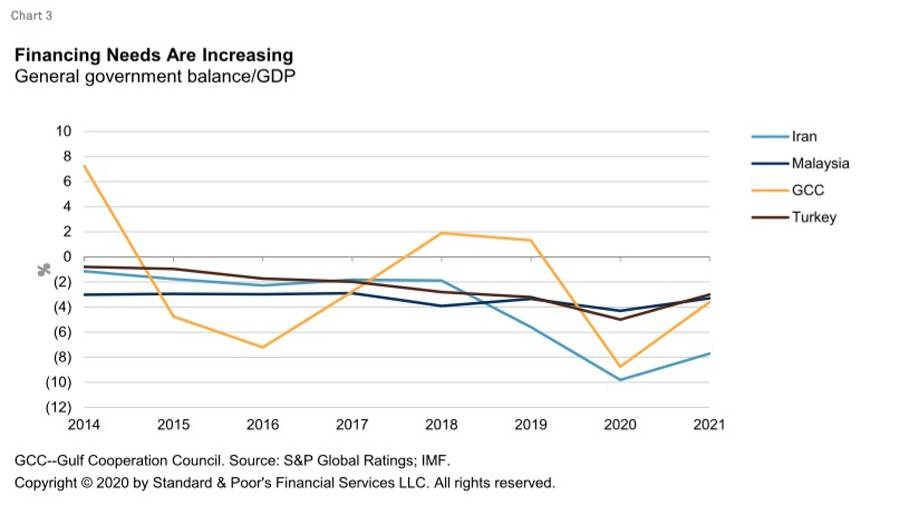

Such measures will result in additional government spending needing to be financed, especially at a time when oil receipts for commodities-exporting countries and tax receipts for other countries are declining (see chart 3).

Islamic finance social instruments could help countries

navigate the economic turbulence wrought by the pandemic

Islamic finance abides by the goals and objectives of Shariah (Maqasid). While interpretations of the Maqasid differ, they broadly center on the protection of faith, life, mind, wealth, and dignity. Until now, in the context of ESG, the social aspects of Islamic finance appear to have been somewhat secondary to the wider climate change and environmental concerns.

In addition to these instruments, we also understand that Islamic banks are considering a more lenient approach concerning their potential headcount reduction, unless the crisis deepens further.

Several conventional banks have already announced that they will retain staff for the time being, but also use other measures, such as paid leave with or without a reduced salary or remote working arrangements.

Stakeholders in Islamic banks could perceive major layoffs negatively and such moves would probably also find some opposition from their governance structures, including Shariah boards.

From a credit rating perspective, as long as the use of social products or a more lenient approach for cost reduction doesn't have a significant impact on banks' profitability, the impact on their creditworthiness would be limited.

Similarly, we would not expect the social nature of a sukuk to have any impact on the instrument's creditworthiness as long as we don't see any changes in the sponsor's financial obligations to pay sufficient amounts for the periodic distribution and principal reimbursement. — S&P Global Ratings