By Christopher Dembik

DUBAI — No theme is more important in the macroeconomic space than inflation right now. All the clients we are talking to share their worries about inflation risk and are looking for investment strategies to hedge against inflation. In recent weeks, we have seen a series of upside surprises in inflation data, that mostly reflect the big imbalances in the economy following the COVID recession and some data noise.

However, we cannot rule out that we will experience in the recovery phase a prolonged period of high inflation due to a sudden change in regime shift characterized by rising protectionism and more redistributive policies to fight against inequalities. If I could give only one piece of advice to investors, read everything you can about inflation and especially stagflation.

There is a large consensus among economists that the initial COVID-19 shock is a massive disinflationary impulse. However, there is no consensus regarding what may come next, let’s say in two or three years.

Some argue that the massive surge in money supply will continue to inflate asset bubbles in real estate and in the stock market, as it has been the case since the GFC, but will have little impact on the real economy as a whole due to the persistent decline of both the money multiplier (the amount of money that banks generate with each dollar of reserves) and money velocity (the rate at which money is exchanged in the economy).

Others fear that in the long run the boom in money supply combined with a regime shift characterized by rising protectionism and more redistributive policies to fight against inequalities will create lasting inflationary pressures and push inflation above the 2% threshold on a sustainable basis. This view is reinforced by the fact that inflation has always been responsive to sudden regime shifts in the past.

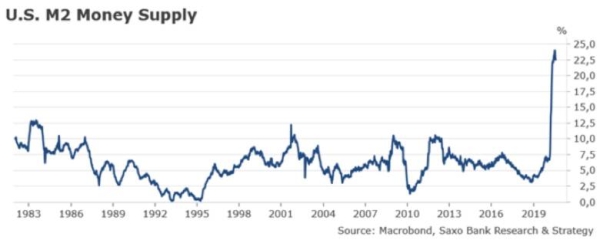

Most economists consider that the most powerful leading indicator for inflation is M2 money supply. It is fair to say that we have never experienced in the past, not even during the 1970’s stagflation, money supply growth as high as it is today in COVID-times, skyrocketing at more than 20% YoY.

We are not there yet. Recent upside surprises in inflation data, such as the surge in US July CPI or the boom in US unit labor cost in Q2, are not linked to the expected regime shift. To be fair, it mostly reflects data noise due to the strict lockdown and the following recession. If we dig into details, it appears that the strong CPI is the consequence of relative shifts in specific markets rather than a general increase in prices.

In regards to the jump in unit labor cost by 12.2% in Q2, it is essentially the reflection of more job losses amongst low-wage workers, thus causing distorting measurements. For at least some period of time, we need to get used to inflation noise and refrain from drawing hasty conclusions regarding immediate change in inflation regime.

It’s all relative. In a very insightful interview to MACROVoices, Vincent Deluard, macro strategist for StoneX Group Inc., proposes another way to approach the inflation problem. He rightly argues that inflation has not disappeared from the real economy over the past years, it is still here, but it cannot be captured by CPI as it measures the average inflation in the economy. Actually, focusing on CPI results in masquering the generational inequality problem:

“The great moderation of inflation in the past two decades has been the result of two offsetting forces. On the one hand, the cost of medical insurance premia, college tuitions, rents in major urban areas, and childcare has exploded. On the other hand, the cost of most of the things, which can be bought at Walmart (and are generally manufactured overseas) has collapsed.

This had led to two very different experiences for inflation: retired boomers, who generally own their homes, live in the small towns and suburbs, shop at superstores and get their medical expenses paid by Medicare have experienced deflation (...). Conversely, new jobs openings for younger generations have been almost exclusively created in major urban areas where costs have exploded.”

Deluard draws two main conclusions:

Generational inequality is prevalent in society. The level of inflation strongly depends on which age group you belong to.

Said differently, the young generations (Millennials and Gen-Z-ers), who contribute most to society based on productivity measure, pay more than anyone else and still face no access to capital to buy home and live properly.

By sacrificing the young and poor to save the old and rich, the COVID-19 crisis has strongly exacerbated generational inequalities and millennial anger against Boomers. One way to solve this issue is for politicians to step in and implement redistributive policies and other popular stimulus programs that can take the form of UBI/Helicopter money.

Now that governments and the US Congress are critical players in driving money supply growth, it is likely they won’t give up anytime soon this new power.

Inflation is always and everywhere a political phenomenon. Its evolution will mostly depend on future policy decisions that will be taken after the crisis. We think that redistributive policies and other stimulus programs will play a key role to create favorable conditions to an inflation episode once the recovery will start to materialize, let’s say in a 12-18 month horizon.

If we combine redistributive policies with the emerging trend of supply chain relocation and rising protectionism, we have a almost perfect inflation narrative for 2022 and beyond that can (temporarily) overwhelms deflationary forces driven by demographics and technology.

— the writer is head of macro analysis at Saxo Bank