By Ole S. Hansen

DUBAI — The post-Nov. 9 surge in risk appetite on vaccine optimism extended into December with stock markets, led by Asia, continuing higher while the Bloomberg Dollar Index, which tracks the performance of ten leading global currencies versus the US dollar, slumped to a 32-month low.

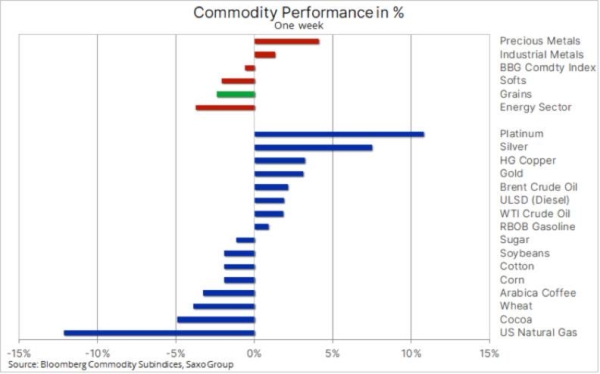

These developments combined with additional stimulus being discussed in the US and Europe and OPEC+ reaching a sensible compromise on post-pandemic production increases helped boost crude oil and metal prices, both industrial and precious.

The agricultural sector paused following a 25% rally since June with cocoa, wheat and coffee the main losers. Scraping the bottom was once again natural gas which slumped by more than 10% with milder-than-normal US winter weather raising doubts about demand at a time of robust production.

Overall, these developments left the Bloomberg Commodity Index close to unchanged in a week that, following the monthly US jobs report, normally signals the beginning of slowing trading activity ahead of the Christmas and New Year period. Still down on the year following the Q1 lockdown-led collapse, the index has made a strong recovery since then.

A trend that vaccine optimism strengthened further this past month and which is likely to be carried forward into 2021. This on the assumption that we will see a strong post-pandemic rebound in growth, the potential for further dollar weakness, rising inflation concerns and weather developments.

All of these could drive the index towards potentially its best year in more than decade and in such a scenario key commodities such as copper, crude oil, soybeans and gold are all expected to perform well.

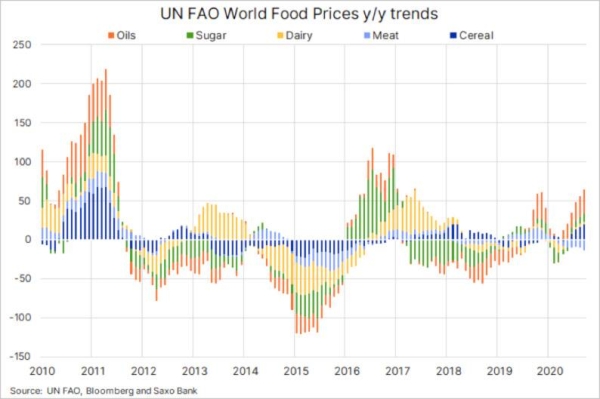

Rising food prices continue to add fuel to the inflation theme which may only strengthen further into 2021 was highlighted by the UN Food and Agriculture Organization in its monthly Food Price Index for November. The index, which tracks the average of 95 food prices spread across five commodity groups, jumped to a six-year high and recorded a year-on-year rise of 6.5%. All sub-indices registered gains in November, with the vegetable oil subindex rising by a stunning 14.5% from October and 31% from the same month last year.

Crude oil reached a nine-month high after the OPEC+ group of producers, following another nail-biting week of discussions, agreed on a compromise deal that will see production rise in stages over the coming months, starting with 500,000 barrels/day in January. With the expected vaccine-driven recovery in global fuel demand this deal will go a long way to ensure the price of oil remains supported until it can stand on its own feet.

The fact that the market rallied despite having priced in a postponement of the previously agreed 1.9 million barrels/day production increase was due to the flexibility of the deal. Meaning that production can be raised but also cut back should the recovery turn out to be slower than expected. Overall, analysts are now expecting that the road towards a balanced market has been shortened and on that basis expectations for higher crude oil and fuel prices into 2021 have been given a boost.

Adding to these supportive developments, a cut this year by the oil majors of more than $80 billion in longer-term capital spending will likely start to feed through to higher oil prices in 2022 and beyond. Unless this past year has changed dramatically the way global consumers will work and travel and thereby consume fuel going forward, only time will tell.

Brent is likely to print $50/b sooner rather than later with already strong Asian demand eventually being joined by others once the Covid-19 cloud lifts. Just how much further it may rally in the short term depends on how Europe and especially the U.S. tackle the current and not-yet-under-control second wave of the Covid-19 outbreak.

Gold recovered strongly from the Thanksgiving drubbing which took the price down to, but not below key support at $1763/oz, the 50% retracement of the March to August surge. While total holdings in exchange-traded funds backed by bullion continued to be reduced, now down 3.7% or 411,000 ounces following the Nov. 9 vaccine announcement, renewed support from a weaker dollar, rising inflation expectations and stimulus talks in the US all helped turn the metal around.

Before these developments, gold was already receiving some support through a copper-linked rally in silver. Copper prices hit the highest in more than seven years amid deepening concerns that miners will struggle to match demand from recovering economies besides the surge in demand already from China. Adding the this, the green transformation which will only continue to increase demand as the electrification wave gathers momentum.

Led by copper, both silver and platinum rallied strongly, thereby helping gold to find support before bouncing on its own merits. Silver had already seen a strong recovery relatively to gold back in August when the gold-silver ratio returned to its long-term average of around 70 ounces of silver to one ounce of gold.

Platinum, meanwhile, needed the vaccine boost and a strong recovery in automobile demand in order to shine. Since these two powerful developments joined forces in early November, platinum has outperformed gold by 20% with the gold-platinum ratio going from 2.15 to the current 1.75.

Finally it is also worth taking a closer look at the copper (LME) – gold ratio and its relative close correlation with movements in US bond yields. The chart below shows that the relationship between the two has broken down during the past month. Copper’s surge higher and fading interest for gold describes a world where growth is the main focus.

Normally, such a development would lead to rising bond yields and the fact that it hasn’t make us wonder whether this is a new normal or whether a realignment can occur. We believe the latter will happen through a combination of higher gold prices driving the ratio lower and a small uptick in bond yields.

We see a risk of rising nominal bond yields with a potential break on U.S. 10-year notes above 1% driving the ratio higher towards 1.5%. However, we maintain the view that rising nominal real yields is likely to be driven mostly by rising break evens (inflation expectations) and not so much by rising real yields as they are most likely to remain anchored close to the current -1%.

Looking at the underlying sources of demand for gold, investment demand may suffer a further short-term setback, but against this the recovery in economic and social activity we may see a revival in jewellery demand, not least from China and India, the world’s biggest consumers. Pent-up demand from a sector which during the past five years accounted for 50% of total demand (Source: World Gold Council) may be lurking following a 40% YoY slump in Q1-Q3 this year.

— The writer is head of commodity strategy at Saxo Bank