DUBAI — On July 8, DP World Limited (DPW, Baa3 stable) announced an offer to acquire 100% of Imperial Logistics Limited, a predominantly African logistics provider listed on the Johannesburg Stock Exchange, for a purchase price of ZAR12.7 billion ($890 million).

The announcement follows the DPW's July 1 news that it was acquiring Syncreon, a North American and euro area specialized warehousing and distribution solutions provider, for an enterprise value of $1.2 billion.

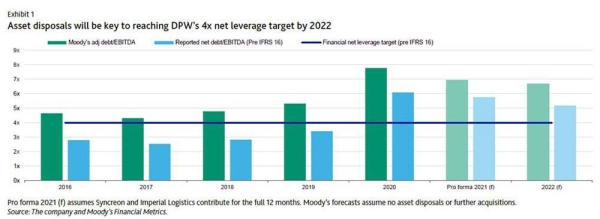

Although both acquisitions expand DPW’s logistics service offering into untapped North American and African markets, they are initially credit negative because they will result in DPW deviating from its commitment to reduce net debt/EBITDA (pre-IFRS 16) to 4x by 2022 from 6.1x as of year-end 2020.

Based on our 2021 EBITDA forecast and including the two acquisitions' contributions for the full year, we estimate that Moody’s-adjusted gross debt/ EBITDA will remain elevated at around 6.9x for 2021, while net leverage (pre-IFRS 16) would be around 5.7x.

DPW's Baa3 rating and stable outlook are unchanged, but assume the company will begin to make significant progress on its asset monetization strategy over the next six to 12 months that would lead to meaningful deleveraging. Downward rating pressure could materialize if DPW continues to pursue a more aggressive financial policy that translates to limited deleveraging.

While the bolt-on acquisitions are not unexpected, they are material. Without significant asset disposals over the next 18 months, we do not expect DPW to achieve its 4x (pre-IFRS 16) net leverage target by fiscal 2022 (see Exhibit 1). DPW is committed to reducing net leverage and we understand that the company is making progress on its asset monetization program.

DPW has sufficient internal liquidity to fund the acquisitions, given it has around $5 billion of available funds at its disposal, including $2.1 billion cash, $1 billion of undrawn facilities at Port and Free Zone World (PFZW) and $1.8 billion undrawn revolving credit facility as of year-end 2020.

Additionally, liquidity will be supported by stable operating cash flow generation, moderate capital expenditures of up to $1.2 billion per year and limited debt maturities over the next 18 months.

Since PFZW raised $8 billion of new debt in May 2020 to fund the minority buyout of DPW and pay a special $5.15 billion dividend to Dubai World, the company has made little progress reducing its reported debt, which totaled $21.1 billion as of December 2020 (consolidated debt plus guaranteed debt at PFZW).

However, the sharp rebound in global trade in the second half of 2020 has led to stronger EBITDA than the company expected, leading to Moody’s-adjusted debt/EBITDA falling to 7.8x at year-end 2020 from 8.2x as of 30 June 2020. Assuming no asset disposals, we expect Moody’s-adjusted debt/EBITDA to fall to 6.6x and net debt/EBITDA (pre-IFRS 16) to fall to 5.1x by 2022. We estimate that DPW will therefore require around $4.5 billion from asset disposals to reach its financial net leverage target of 4x.

US-based Syncreon provides specialized warehousing and distribution solutions and generated revenue of $1.1 billion in 2020. Its long-term relationships with blue chip customers and high contract renewal rates provide good revenue predictability. Imperial Logistics generated revenue equivalent to $3.5 billion in 2020 and has leading market positions in South Africa and established routes to other African countries.

Imperial Logistics provides an important gateway into Africa doe DPW, allowing DPW to be closer to its end- customers on the continent. However, operating in Africa is risky owing to more difficult operating environments including volatile local currencies which translates into less predictable cash flow.

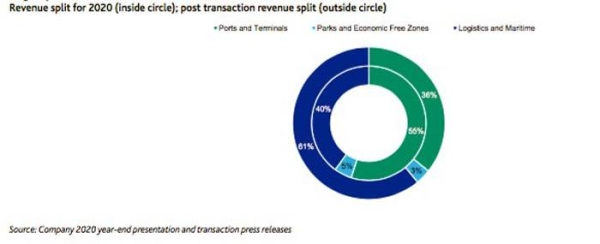

Both acquisitions will materially increase DPW’s proportion of logistics and maritime revenue to around 60% from 40% (Exhibit2). However, DPW's ports and terminals and parks/economic free zones segments will still contribute the bulk of EBITDA, which we estimate will be at around 70%.

This is because the acquisitions will be margin dilutive, with DPW's pro forma EBITDA margin falling to around 30% compared to 37.2% for fiscal 2020. Despite the lower operating cash flow, the asset light business models will support positive free cash flow generation.

Both transactions are subject to customary completion conditions and regulatory approvals, with Imperial Logistics also subject to its own shareholder approval. Syncreon is likely to close in the second half of this year and Imperial by first-quarter 2022. — Moody's